Contango Ore Publishes Strong Economic Assessment for High-Grade Johnson Tract

Johnson Tract could end up being CTGO's crown jewel. High-grade. Lots of exploration potential. Cheap to get to production. Pretty good adjectives for a gold project.

tl;dr:

Positive news out of Contango Ore recently (CTGO.NYSE), with their initial assessment (PEA) for their Johnson Tract project freshly announced this week.

Economics are predictably strong, including post-tax a 1.3 year payback and 30.2% IRR

CEO Rick van Nieuwenhuyse and CFO Mike Clark joined 6ix on May 8 for a panel update on this news.

Below you will find that video, my thoughts on the news, and a written summary of the panel.

Content Order: 1. 6ix Panel Video, 2. Overview, 3. 6ix Panel Written Summary

Note to Readers

CTGO is a solid company with potential for substantial growth over the coming months and years. This is a good one.

If you’re feeling inclined, please support me by clicking through and subbing to their newsletter to demonstrate to them the following I can muster.

I generally prefer to avoid this sort of direct promotional labour for me, but I will never deny the importance of acquiring data.

Please Click Here To Support Me By Subscribing to CTGO’s Newsletter

Thank you.

1. 6ix Panel Video

If you want to watch the video for yourself, you can do so below, or read on for my overview and summary.

2. Overview

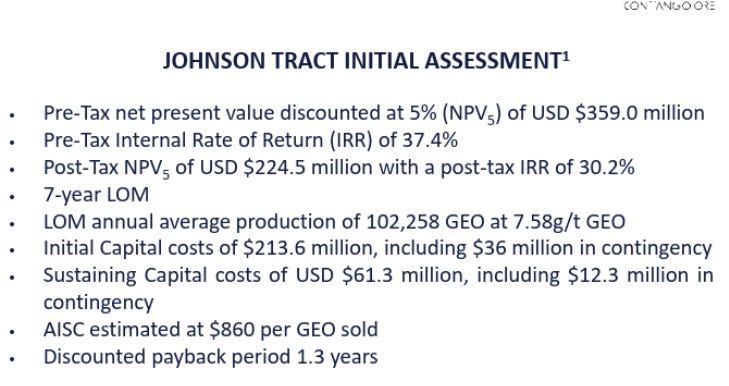

Contango Ore put out the first economic assessment for their Johnson Tract1 Au+Ag+Zn+Cu-Pb deposit in southern Alaska this week. And the numbers were solid. With about 700,000 recoverable gold-equivalent ounces (GEOs) over the 7 year mine life, John Tract is a step up in both annual production and LOM from currently-operating Manh Choh.

Now, the full report isn’t out yet. (There’s one distinction with the US listing - whereas Canadian-listed companies have 45 days to release their report after it is announced, US-listed companies have only 4.) So it should be out this coming Monday at the latest if my math is mathing. So for now we only have the highlights to work with, but see below for yourself. These are good numbers:

And remember, there’s very reasonable beliefs - as have already been seen with Manh Choh - of the full size of the deposit being quite a bit larger than these initial numbers - recall here that due to the location of JT (nestled uncomfortably within a mountain) just getting it properly drilled is a challenge. Mineralisation is open both above and below the current deposit.

Anyway, I will give the brief highlights of the report below and then provide a more complete summary of the 6ix panel on its own after.

The Highlights

Base case of $2200 spot

Boilerplates are good (below all base case):

Post-tax IRR of 30.2%,

Payback period of 1.3 years.

NPV5 of $224.5M.

AISC of $860/oz

Even with royalties and taxes it should still be sub $1000 as per CFO Mike Clark

Initial capital of $213.6M.

NPV5:Initial capital (IC) ratio of 1.05 using base spot, so good enough.

Cheap initial capital costs - easier to finance.

Sustaining capital of $61.3M. Very cheap.

LOM Revenue (NSR less Royalties) of $.297B

70% of revenue will come from the gold.

One thing I appreciated: Large contingency allocation - 20 on sustaining capital and 25% for initial capital.

Not playing numbers. Can be very easy to make a hand wavy PEA with 10% contingencies only for costs to balloon 50% once things get serious at the feasibility stage.

Leverage to Spot

At $3000 gold, post-tax NPV5 balloons to $398.2M,

This gives us an NPV5:IC of 1.86

At current spot of ~$3300 it is ~$465M.

Which is an NPV5:IC of 2.18.

However, even at $1800 gold, post-tax NPV is still ~$140M, so there’s some durability here.

Point is, it’s a good time to be a gold producer.

Highlighted Data Tables

Here’s the data provided in the news release, highlights my own.

Conclusion

Contango is a smart play with a strong idea. Manh Choh has them making good money and aggressively paying down their debts and hedges. Has to be a good feeling to be a gold producer with gold at all-time highs.

However, I get the sense the market is stuck a bit in “prove it” mode with them - waiting to see if Johnson Tract and/or Lucky Shot can be advanced on time and on budget to build upon what they have at Manh Choh, or if delays and disruptions will rob this company of its true potential.

I’ve spoken before - the strength of the “direct shipping ore” (DSO) model Contango employs is it allows these small, high-grade deposits to together be greater than the sum of the individual parts. But that only happens if plans can be executed effectively. With such narrow mine life windows and time-consuming permitting and construction processes, execution matters here even more than it generally does.

But I see a company that executes and a leadership team that knows what to do and how to do it. The bridge problem has been incrementally minimised while we now wait for the bridge repairs to take place. Manh Choh went into production on time and on budget. They beat production forecasts. Their production cost estimates are accurate (again, I like those fat contingencies they used). They pay down their debts in advance.

Every piece of evidence I have suggests Rick and the rest of the Contango team know what they’re doing. There have been some frustrating hiccoughs, yes, but they were navigated and this story and its long-term vision and potential remain largely intact.

Johnson Tract is a key part of that long-term vision. And with the (strong) economics on it now released, plus the very good chances for easy resource expansion, it is easy to understand why.

So yeah. The market is either sleeping on this one, or has outsized fears regarding execution.

I feel otherwise. Yes parts of Contango’s expansion plans are a bit more of a slow burn (crazy that 5 years till production is considered remarkably fast), but, come on, they’re producing gold at all-time highs. They are bringing in 10s of millions of dollars right now this year with Manh Choh. And if they can achieve their goals over the coming years, Contango’s market cap will almost assuredly be multiples from now. All will be forgiven if Contango can prove it has what it takes to make it all happen.

From my perspective the reward is more than worth the risk.

Read on below for a summary of the 6ix panel discussion CEO Rick van Nieuwenhuyse and CFO Mike Clark participated in on May 8 wherein they discuss and answer questions about this news release.

3. 6ix Panel Written Summary

Note this is not strictly chronological. I worked to organise the panel under various topics, rather than by time stamp.

1. Basic JT Intro

(Click through here for a brief overview of JT or here for Contango’s own overview.)

Studies for road to port site placement, and the port site itself, are ongoing.

Portal road is permitted.

In process of permitting location for portal.

Tunnel/ramp will be simple and cheap. Straight, relatively flat (5% grade), 1.5 km long

2. Benchmark Numbers

1.3 year payback (impressive)

Grade and long-hole stoping drive this.

AISC of ~$860.

Include royalties etc. and it will end up somewhere just south of $1000/oz.

Gold is 70% of revenue.

UG mines of course need to spend more money before OP to get to revenue.

Even at $1800 gold, post-tax NPV still of ~$140M.

Sensitivity chart below

3. Mine Plan and Construction

Putting all the mine workings in the hanging wall.

HW is barren - post-mineralisation intrusion. Dacite.

This means you aren’t messing with ore-grade material, but also that it being sulphur-free means no risk of acid leaching.

Enter mineralised footwall at the bottom and work up.

The thickness of the deposit is beneficial. Makes stoping possible.

Hope to begin production in 5 years. Feel that is reasonable, and hopes for earlier.

Justifies using an NPV5.

Actually begin mining in year -2.

Fledgling production begins in year -1.

Optimisation Potential

Continue to look into ore sorting.

Would be a strategy to help weather crash in gold price.

Otherwise, fuel for transportation and labour are two of the biggest expenses.

4. Cost

Roughly 50% mining, 25% milling, 25% G&A and transportation

Initial Capital of $213.6M

$15 million for tunnel, resource drilling, road to portal.

Need 10-15,000M of drilling to get it fully ready for mining.

$36M contingency (25%)

Sustaining Capital of $61.3M

$12.3M Contingency (20%)

5. Capital Allocation Strategy

Debt and hedges remain priority.

$30M in debt remaining.

Hedged ounces were ~125,000 in July and are now ~75,000 remaining.

Will look to fund JT with some amount of debt financing.

Unencumbered, Manh Choh would be doing $100M in annual FCF.

By the time construction is set to begin, Manh Choh will be unencumbered.

However, don’t want to spend all money on just JT.

Will work to avoid hedging this time around.

Next round of funding with banks will be a better process.

Paying off Manh Choh demonstrates their viability.

So too will the $100m in annual FCF.

Potential for Future JT Resource Growth

The nature of where JT is physically located means drilling both above and below the current deposit isn’t feasible.

UG workings will give CTGO access to drill up to surface and deeper down as well - very reasonably optimistic that both directions will add tonnes to the mine plan once they are able to actually access them.

Grade Dilution

Resource is 9.4 GEOs /tonne.

However, mining dilution drops it to 7.58 g/t by the time it is milled.

UG mining is a a matter of understanding the tradeoff between cost-to-mine and amount of ore loss/dilution.

Primarily relying on long-hole stopes in current plan

However, sublevel caving (more tonnage/less precision) or Room and Pillar might also be an option.

Needs more technical work to determine ideal plan.

Ore Processing Partner Update

Five different potential partners for JT.

Shipping of course is cheap and provides lots of optionality.

One partner even just wants to take the ore and ship it across to Asia to be refined there.

In that scenario, they’d likely just sell JT to the partner as that' isn’t a process they want to get involved in.

Ore will be transported and contained 25T per shipping container unit.

Makes for easy transit - can be moved by machinery, stuck on trains, etc.

Also prevents contamination, ore loss, reduces dust impact, etc. vs. stockpiling.

US-based, so an S-K 1300 initial assessment, not a PEA.