"The Power of Discovery": A Conversation with Sitka Gold

VP Corp Dev Mike Burke of SIG.V joined me during Vancouver conference season to talk about why 2025 is such an important year for Sitka.

Here's a video on Sitka gold I produced while attending AME Roundup 2025 a couple weeks back. Look for a longer video on the Vancouver conferences to come out in the next week or two.

Sitka Gold (SIG.V) is a Yukon gold explorer I came across a couple years back and liked them - good jurisdiction, good potential - but never followed up with properly and they gradually drifted off my radar. But recently, I've rediscovered them, and at a good moment in good time, too - an impressive recent resource update and a large, 30,000m, campaign slated for 2025 has Sitka at a very exciting stage in its development - that hopeful, blue sky expansion from one or two discoveries into 3 or 4 or 5 or more that drives a company's rerating.

VP of Corporate Development Mike Burke joined me for a few minutes while we were at AME to talk Sitka, what it has, and what it is building, to preview a potentially transformative year for Sitka.

Content in three parts: 1. The Interview, 2. The Companion Article, and 3. The Written Summary are all below.

Part 1: The Interview

Part 2: The Companion Article

I wrote about this in my “JRI In Review”, but there’s an investing sweet spot in a project’s life cycle where a solid initial deposit has been fleshed out, and, lessons learned and models honed, the next step that companies either ascends or falls on is to identify and target anomalies to drive new discoveries and new deposits and turn an interesting 1-2 million ounce project into a 4 or 5 or more million ounces.

Being able to identify companies that are able to make that jump prior to them doing so has been a high percentage game for me so far, and I am inclined to believe it’s a good overall spot to enter a position. You remove the risk (and, yes, also the reward) of discovery and that initial run up, but if you’ve got an effective filter, the reward from this point onward is 1. Sizeable and 2. Substiantially derisked. I’ll take a 75% chance of a 3 bagger over a 10% chance of a 10 bagger every day of the week.

So what are those traits? Funnily enough, there’s always evidence that makes it easier than you might think. Here are some things I look for:

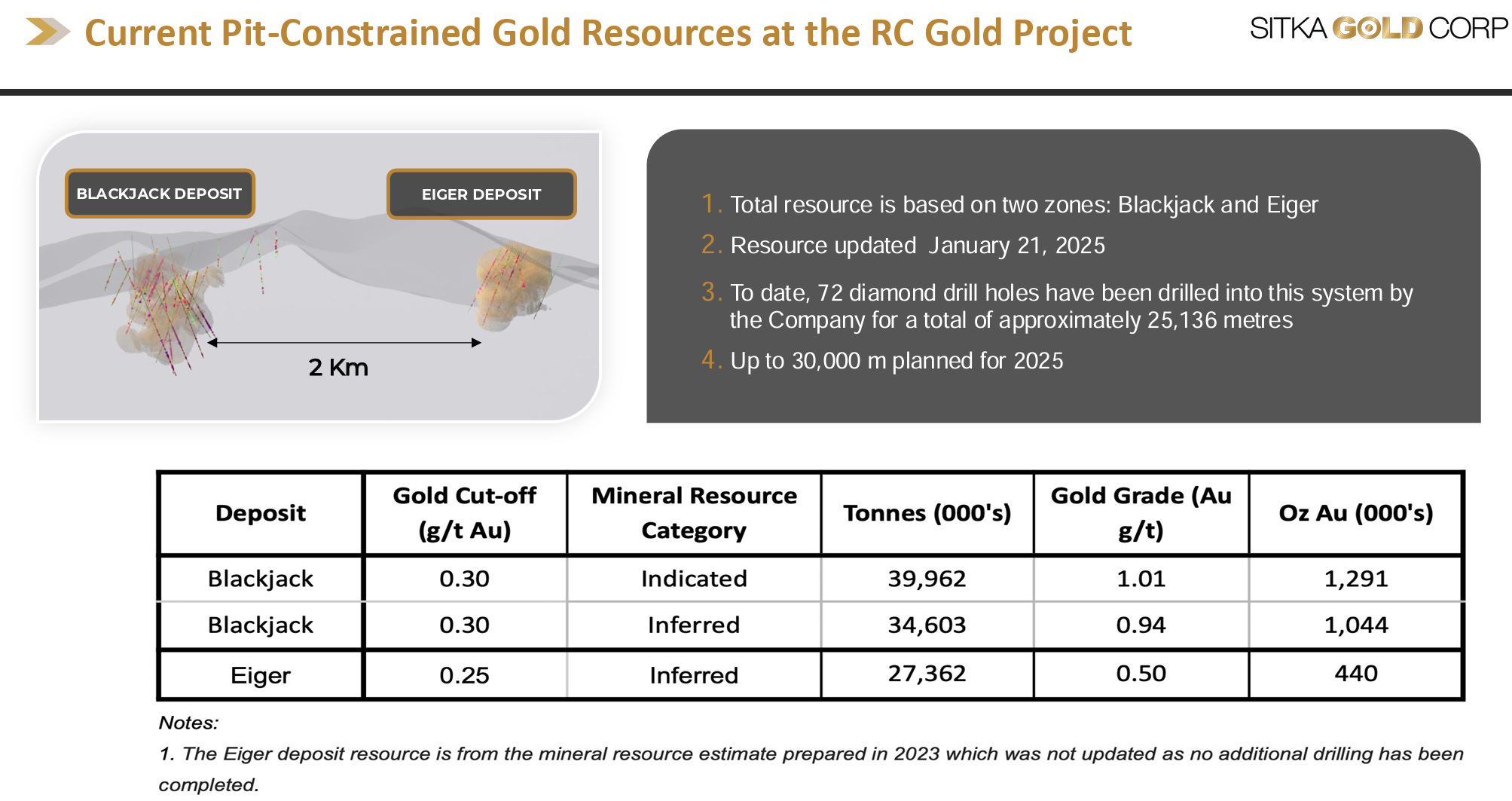

First deposit is a clear success. Grade, tonnage, and/or continuity all clear wins. Companies drill their best (known) targets first. Good luck happens, but it is important to start strong. 2.3m oz at Blackjack (and 2.8m oz overall) means Sitka checks this box emphatically.

The rest of the land package has clear potential. Geophys anomalies, anomalous grab sample grades, channel sampling, historical holes, etc. The market doesn’t generally give credit to smoke, but if you can read the signals you can fairly reasonably make assumptions about the fire itself before it is formally discovered. Not to torture an analogy. Sitka has holes drilled with singificant lengths of strong mineralisation at quite a few targets that are just begging for further discovery and expansion. You can’t get a much better clue than that.

Clear evidence of strong ability to raise funds. Sitka raised $5.5m in early September on a half run and the stock immediately started a run to 50+ cents by late October. Then in November they announced a $5 million flowthrough with no warrants attached. So with limited potential overhang Sitka has fully funded their 30,000 meter campaign for 2026, keeping the runway for share price appreciation unemcumbered.

Related to #3 - lots of drilling announced and fully financed. There will be always be another financing, but knowing the big, exciting, “level up” drill campaign is ready to roll means that sentiment and excitement get to run more freely. 3 rigs and 30,000 fully financed (more than doubing all Sitka meters ever drilled) meters is exactly this.

Institutional and analyst interest. This isn’t absolutely essential, but typically reflects market interest and attention (and thusly potential to get credit for your work). Michael Gray and Agentis, as well as Paradigm Capital, both provide coverage and Crescat, Canaccord, Sprott and others show significant institutional support.

Now, yes - the float here is big. 340ish million shares out. And yes, ideally projects get to this stage with a big smaller float, but this doesn’t bother me as much here as it might elsewhere:

They’ve got lots of other things going for them that help that be less of an issue. Quality does have a tendency to shine through. (AbraSilver and Dolly Varden are good examples of this from my companies I cover - truly good projects aren’t defined by their share counts).

The actual risk of larger share counts is the fear that the shareholder registry has gotten out of control a bit and there are more traders and warrant clippers than actual loyalist investors involved. This in turn produces significant churn that can turn good news releases into liquidity events rather than share price catalysts. However:

This doesn’t seem to be an issue for Sitka. Chart looks like it is responsive and healthy enough based on the recent run-up and - most critically - there isn’t anybody trapped in positions looking to unload. The last year is one big ATH for Sitka. No weight on the stock up here.

All these attributes that I believe points to a company being able to make that critical leap in size I spoke of at the start are present with Sitka. And the timing couldn’t be more perfect - 30,000 meters of drill produces a lot of news flow. And we sit on the precipice of that news flow now.

So I was glad of the opportunity to sit down with Sitka’s VP CorpDev Mike Burke at this recent AME Roundup. His personality, as well as his passion and knowledge about Sitka and its RC Gold Project was infectious and reassuring as a sector participant and investor.

I keep doing more digging here trying to get properly acquainted, and the more I read the more I like. I officially own about a half-sized position in Sitka and am open to more as my DD process continues.

All signs point to Sitka having an excellent chance at a rerating through drill bit growth in 2025 and becoming a true M&A candidate. And for me, that’s a pretty darn good investment thesis.

Part 3: Written Summary

Timestamps are links to the interview

00:10 Introduction to Sitka and its 2025 plans

New resource: 1.3M oz indicated, 1M oz inferred

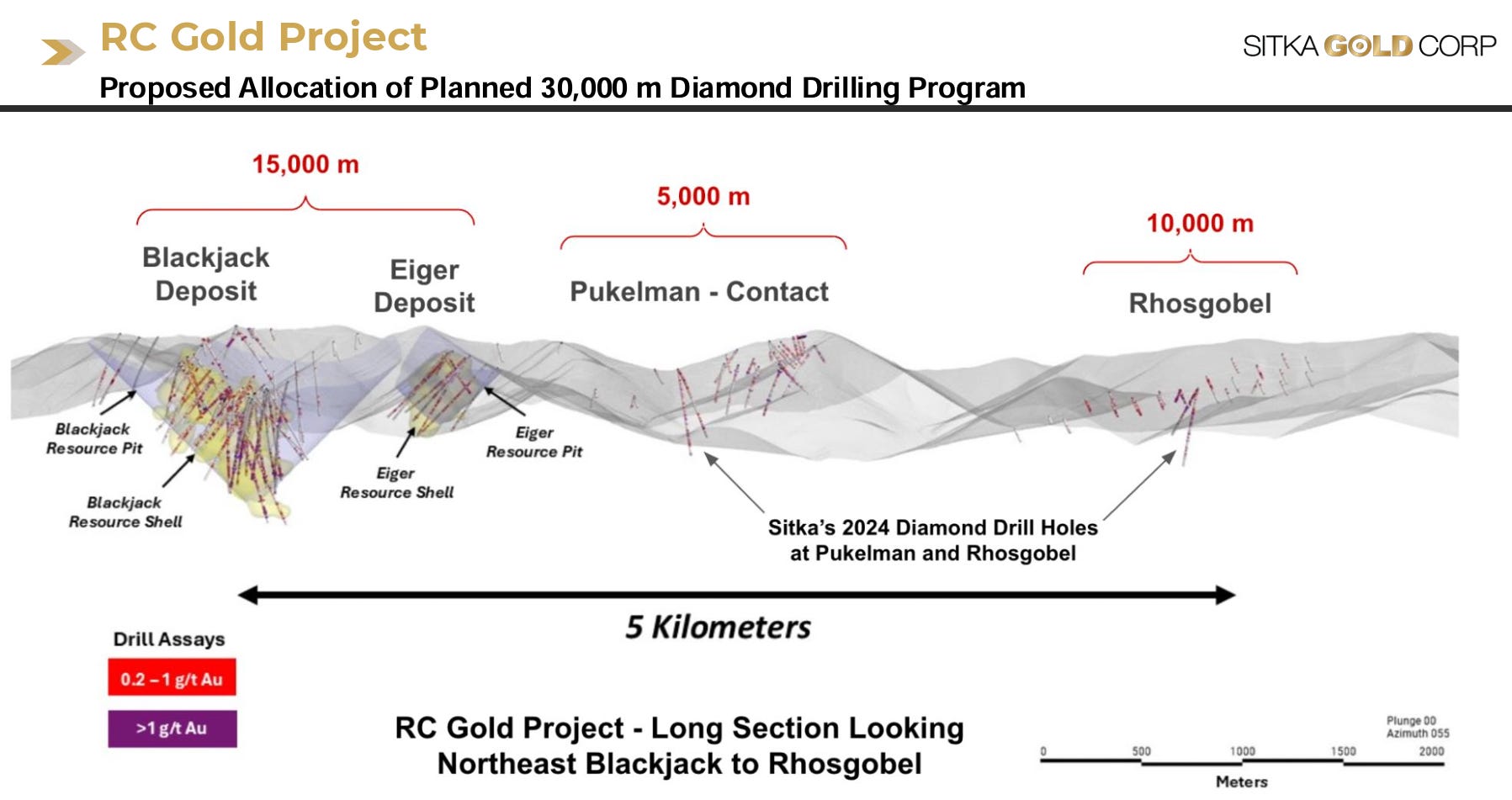

Three rigs targeting multiple zones across property with 30,000m this year

Rhosgobel getting 10,000m - largest program component

Pukelman allocated 5,000m for initial testing

Both zones targeting maiden resources

Building on successful Blackjack model

Systematic approach to testing regional potential

Clear Creek complex showing multiple opportunities

Multiple mineralized intrusions identified

Blackjack initial resource built on 7,500m, then 11,000m more than doubled the ounces

Resource growth exceeded initial expectations, Quality of mineralization remaining consistent

System showing remarkable continuity and Multiple zones still open for expansion

Rhosgobel represents largest exposed intrusion and has Extensive 1.5km by

500m target zone identified. First-ever diamond drilling now planned

Pukelman showing 500m mineralized corridor

Multiple untested zones between known areas

07:49 Technical Parameters

Raised cut-off grade from 0.25 to 0.3 g/t for the new resource

Strong geological model driving drilling decisions

Grade consistency supporting resource confidence

Structural controls well understood

Deposit characteristics matching regional analogs

11:43 Metallurgical Progress

Initial bottle roll tests showing 94% recovery

Confirmed non-refractory nature of mineralization

Additional studies examining milling potential

Gravity and cyanide leach testing ongoing

Matches well with similar deposits in region

Results supporting development pathway

15:47 Future Exploration Plans and Potential

Hole 68 hit 680m at over a gram, Including impressive 93m of ~2 g/t at depth

Planning to reenter holes and wedge off them to save money.

Among deepest holes in these system types

Underground potential becoming interesting

Testing plumbing system and source potential, High grades at depth opening new opportunities

Vertical extent remains untested, Wedge holes to reduce drilling costs

Multiple targets showing Blackjack characteristics

Similar deposits in region typically 3-5M oz

Cluster of intrusions all around 93 million years old

Suggests common mineralizing source

Gold coming from depth, testing deeper potential

Strong infrastructure supports aggressive program

Steady news flow expected through 2025

Clear pathway to demonstrating district potential

Moving from single deposit to regional exploration

Multiple catalysts upcoming

19:40 Strip Ratio Discussion

Can't state officially in resource calculations

Analyst reports available with estimates

Any potential suitors can run their own numbers

Open data access supporting valuation

Conservative approach to technical reporting