"JRI In Review", Pt. 1 of 2: Returns-to-Date and Discussion

After nearly 3 years, I've calculated the returns-to-date of "JRI: The Portfolio". Part 1 here focuses on a general intro and overview. Part 2 will showcase all companies to-date and thoughts on 2025.

tl;dr:

After the better part of three years of doing this, and two years of it as my full-time gig, I figured I would finally do a deep dive on my own work and crunch the cumulative returns of the companies I have interviewed since my inception and see how they stack up next to various sector and market benchmarks. No gimmicks, no tricks, no fudging of numbers. Just data, transparently provided and analysed.

However, 3 years and over 100 interviews is a lot of data and this project simply grew too big to keep as a single article. So below you will find part 1 of 2 of this “JRI Returns-to-Date” project. This first article has in it: 1. An Intro, 2. An Explanation of my Methodology, 4. A General Overview of my returns and, finally, 5. A conclusion.

Part 2 meanwhile will consist almost entirely of a company-by-company break down (the missing #3 from above) as well as some final reflections on my work so far and what 2025 has in store.

And if you don’t have time to read on to learn how I did? Let me just say it here: Pretty damned good. Here’s the headline numbers:

Total Portfolio returns came in at 44.7%, tying GDX while beating all other major sector benchmarks. And even better, my Core Portfolio (companies I have worked with the most) is up over 58%, beating out all benchmarks, including gold spot price and SPY itself. Which I happen to think is pretty damned good. Lots more stats below.

Index

1. Introduction

2. Methodology

3. General Review

4. [In Part 2: Company-by-Company analysis]

5. Conclusion

This update is the result of nearly four weeks of collecting, collating, calculating, comparing, analysing, writing, editing and creating have been spent building this update on the past (nearly) three years of my work. If I am going to build a universal update on JRI since inception? Well, a job half done is as good as none. No half measures, but maybe halved articles. So welcome to Part 1.

Though it is a little bit solipsistic and/or navel-gazey to analyse my own analysis, I don’t think it’s wasted efforts. Proving clearly and emphatically what you can do - in the ultimate “show me” arena that is the market - seems critical to anyone trying to play the game in a serious way.

Consider that the whole point of being a stock picker/analyst is, at the risk of sounding redundant, actually analysing and picking stocks. Have you got “it”? Have you - some how, some way - developed the edge, the knack, the know-how, the instincts, needed to actually beat the market? Most never do.

Now, if you don’t actually have standards, there is a relatively straight forward way to game this market to your advantage. Buy some followers and like bots from the engagement farm of your choice to build the illusion of legitimacy, master SEO and marketing techniques, and proceed to hype any company willing to pay you to do so.1

Under such a model, your actual analysis, picks, and returns aren’t the point, because your prowess as a stock picker isn’t the point of your business model. Rather, the slick marketing and your ability to always find another company another view, regardless of the quality of either, is how your make your money.2

. The background is cluttered with bright, clashing colors like neon green and hot pink, with absurdly oversized text saying 'YOU WON'T BELIEVE THIS!' in bold fonts. Random props like money, arrows, and explosion effects are scattered chaotically. The design is overly loud and garish, evoking cliched clickbait aesthetics.")

And hey, even if you burn through your real followers you’ve managed to attract, who cares? There will always be a new wave of rookie investors looking for riches to try to ensnare with slick marketing and flashy promises. You and the unscrupulous companies you work with know this all too well.

To start making my way back to my original point: What I have described above - common as it is - importantly is not the game of stock analysis, but of stock promotion. Sure, success takes some combination of both, but which one is driving the car? The correct answer should be obvious.

The fact is, if you want to build a real reputation as someone worth listening to and listened to seriously… well, you gotta bring the goods. Which has nothing to do with how well-known you are or how many companies you’ve covered, or how sharp your thumbnails and post-production is. It means you gotta beat the market, or at least your sector benchmarks, or what’s the bloody point?

So that’s why we’re here. To see how I stack up.

But, as with everything, it isn’t what you’ve done, but what you’ve learned from it that matters. So to that end, yes I have data and stats - both collective, portfolio stats and also company-by-company results. But, maybe more importantly, I have tried to highlight “lessons learned” from companies as I go. Understanding your own successes and mistakes - and what you did or didn’t do to make them come to pass - is the key to self-improvement. And if this is what I want to do I need to take it seriously.

And to be clear, though exhaustive, this is still just another data point. No doubt some names here will see their stories change and there fortunes reverse, for goodor ill. Two and a half years of work is a decent track record, but it’s still an arbitrary finish line placed upon companies whose projects can take years to unlock.

So here we go. No bullshit. No obfuscating or hiding or . Just results and reflections on those results.

2.1. Intro, or, “Thoughts on Bullshit”

Anyone who has even lightly engaged in statistical analysis knows how shockingly easy it is to produce wildly different results on a particular subject based only on 1. what dataset(s) you did/didn’t use and 2. what exactly you did with that data. Bad data produces bad data, and bad analysis produces bad data. Whether by ineptitude or malice, garbage in is garbage out.

And let’s be clear, here. This ability to massage data to say what you want it to say can be dangerously effective weapon. And, obviously, if you do what I do (stock analysis and promotion) you are very much incentivised to skew your metrics in such a way that maximises your apparent performance as a stock guru.

For example - one of the go-to “lies, damn lies, and statistics” that pumpy, low-quality stock gurus like to utilise is focusing solely on “peak returns” - what was the highest the ticker in question traded since coverage started?

Pumpers love posting cumulative peak returns as some breathless display of their stock-picking prowess. Because it is always invariably a really big number that naturally hooks people’s attention. But that is almost always deeply (and intentionally) misleading.

Now, there is unquestionable value in knowing that number. Maybe it’s unrealistic to expect to nail the top, but knowing the window for potential gains - and how big those gains could have been - does mean something fairly important. Being nimble and knowing how to read and play momentum is important, especially so in the micro cap world. And even more so in a tough/sideways market like the junior resource sector is currently in.

But it also clearly doesn’t tell the whole story - a buy call made a year ago at 50 cents that peaked at a dollar a week later for a couple days before crashing permanently to 5 cents… well that theoretical 100% gain doesn’t quite tell the whole story, does it? And I don’t think people trapped in that trade would agree very much with stats painting it as a win.

So, is peak returns a valid piece of data? Absolutely. And an important one even. But, like essentially all knowledge, it needs other critical pieces of contextualising information for it to be properly understood, and in the absence of that context can be downright misleading.

And there’s a word for highlighting single datapoints cherrypicked to fit a pre-determined narrative (in this case, that the author is some master stock guru):

Bullshit.

If you’ve followed along with me and my work for any decent amount of time, I hope it is obvious that a core goal for me all along has been to cut through the bullshit this sector can produce and not create any more bullshit myself. So when it comes to doing some sort of “universal JRI returns” update… I need to be objective and transparent about my numbers and how I arrived at them.

Secretly applying a narrow set of filters intended to produce data to support a predetermined hypothesis is pure-strain bullshit. You’re effectively lying to everyone at this point - even yourself.

But realistically, bullshit can work for a while and bullshitters can build a lot of success and a serious following through use of that bullshit. Slick marketing and content can deny reality for a good amount of time.

And if you ask me, that’s the standard, expected norm for people who do what I do.

But reality can only be denied for so long before it always and inevitably one day when comes crashing through your roof on you.

So first and foremost, the goal here is to be realistic, open, and accurate. In other words? No bullshit.

2.2. My Aim

My goal was pretty simple. I wanted to know how my companies I have interviewed have fared to date as if they were positions in a hypothetical “JRI Portfolio”. Treat the share price on the data of first interview as a “buy”, compare it to now, and add them all up. That’s the simplest version of it.

However, this “equal weight” approach felt incomplete. Should companies I interviewed once two years ago count the same as companies I’ve written about or interviewed a dozen times? Intuitively, that felt wrong (though I provide that data for you to see).

So a simple, fact-based, weighting method to simulate high-conviction companies was used. Obviously, weighting systems can provide cover for thumb-on-the-scale shenanigans, but if done properly they also more accurately reflect the composition of a theoretical resource exploration fund.

I felt that so long as the weighting rationale was transparent, logical, neutral, and consistent, that it would likely more accurately convey a sense of not just how the companies I have covered have done, but of how companies I had conviction in have done. Because if I like them enough to keep working with them, that should mean something, right?

Put simply, my belief was that if I have worked closely with a company, whether their returns are good or bad, I need to wear those returns in a bigger way than one-offs.

2.3. My Methodology

I treated the date of publication for my first interview with a company as a “buy” using the SP from that day. I felt this was clean, simple, objective. Hopefully you agree.

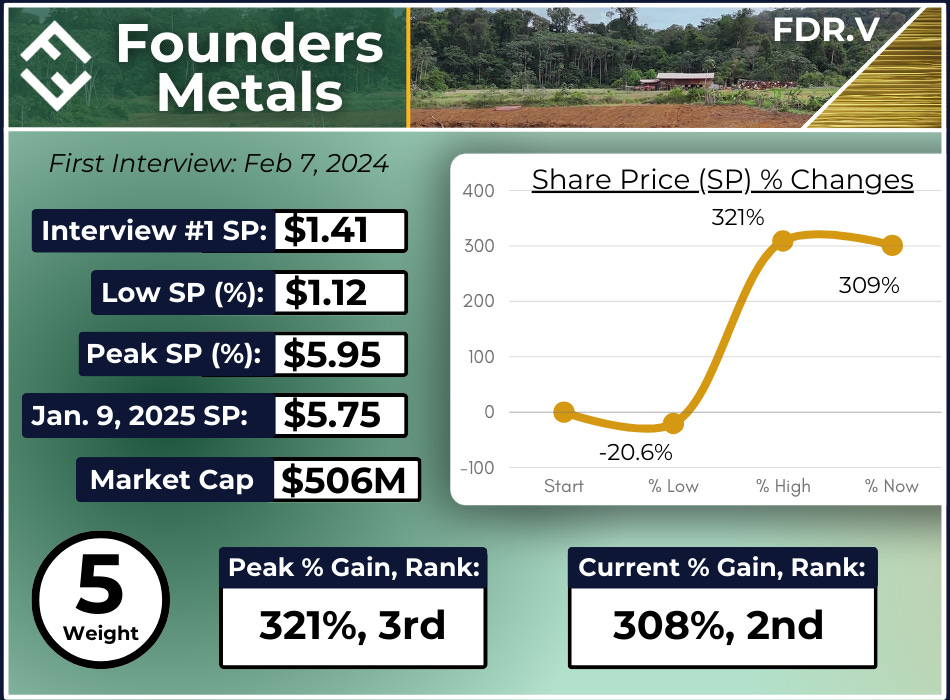

I used a weighting system that aligns with the amount of coverage I have provided for a company. Basically, more coverage = a bigger position. Check the infographic below for more on the weighting, but it is a basic system of 1 to 5, that directly correlates with number of interviews/amount of coverage, but with a grade cap of 5.

Companies with a weighting of 3 and up are considered the “JRI Core Portfolio”.

This runs from July 28, 2022 to Jan. 9, 2025. It’s my third end date I have calculated for. The first felt like I was unduly capturing a downswing. The second felt like I was unduly capturing an upswing. January 9th felt like it captured more effectively the median in the natural variance of a portfolio that aribtrary end dates can

In “Section 4: Company Discussions” I’ve broken down the companies into 4 categories: “Wins”, “Losses”, “Draws”, and “Too Soon to Tell”. Anything +/-20% its starting price in this volatile sector I considered a draw, regardless of my feelings towards the company. Note that regardless of their category, the weighting system and returns does not change. Just my discussion of them.

My fourth category - “To Soon To Tell” - might be a bit of a cop-out if you don’t feel like being generous. I wanted to provide space for companies I remain high conviction on but whose share price have nevertheless suffered since I began following them. Note that only “Core Portfolio” (weightings 3-5) companies are on this list. I feel like that warrants some distinction from a pure “Loss” in terms of how to approach them.

I am going to try to let the infographic do the talking. I’ve got more than enough to talk about in the company reviews to spend , which I will release in a few days.

But the quick and dirty version? I think I am doing something right. I want to repeat this a few times, because I want it to sink in:

I beat the market.

(Either slightly or significantly depending on how you look at it.)

The Headline Numbers

1. Total Portfolio returns (44.7%) either meeting or exceeding industry benchmarks.

2. Core Portfolio3 (58.1%) significantly outperformed: Gold spot price by nearly 10% (53%), SPY by nearly 20% (48.9%) and assorted industry benchmarks by some 30% - 100%+. Graph below.

3. Average per-company peak gains an impressive 117.1%

4. 1 in 8 picks peaked at 4X or more, with a current average of 5.3X.

3.1. The Infographic

3.2. Quick Hit Thoughts

Here’s a brief run-down of numbers and observations that stand out to me from my time with the data.

3.2.1. Hold Your Winners, Dump Your Losers

The data provides a clear lesson often taught in this sector - hold your winners and dump your losers, though it feels counterintuitive to some. Consider:

A small handful of companies have an outsized portion of the gains in my portfolio - 80% of its value is held by just 31% of the companies. But that’s the whole point of the junior resource sector. You will lose. Often. The secret is knowing how to recognise the multi-baggers that define this sector to make up for those losses. So the fact that my portfolio has ended up top heavy - 1 in 8 of my picks have peaked at 4x or (much) more to date - is very much a feature not a bug.

Some stats to back “hold winners, dump losers” up:

Just less than 1/3 of my companies doubled.

The average peak of those companies that doubled was 3.3X

It is important to note that the vast majority of those returns came from 4 companies who averaged nearly 6.5X peak returns between them, including one (intra-day) 10-bagger.

The remainder of my doubles aside from these had an average peak of 136%

Of the companies that doubled, only 1 in 10 ever went below a low -31%.

Of the companies that doubled, only 1 is currently in the red (-5.6%), and another is only moderately green at +35%. The rest approach and exceed +100%.

Conversely, companies who went down generally never went up.

2 in 5 of my picks are currently down -65% or worse. Their average peak was just +35%.

This average is skewed up by a few near-double outliers. I will discuss this little category of “winning losers” on its own later.

Concerning all-time lows, once a company seemed to hit -40% from my first price, their odds of recovering went way down. Only 22% of companies who exceeded -40% ever recovered more than 10-15%, with most continuing on down to greater losses.

Only 1 single company I covered ever went green from being -40% down or more.4

3.2.2. Traders’ Delight

This portfolio had wild amounts of beta, unsurprisingly. Only 1 company (Fireweed Metals) had a less than 50 percentage point swing in their share price.

I’m going to go ahead and assert that if you aren’t swing trading - or at the very derisking in tranches to capture gains during runs - you’re assuming far too much risk regardless of your returns.

The average peak return of all companies was a remarkable 117%.

If you remove the top and bottom outliers, the middle ~70% of companies averaged a peak of 72%.

This means if you followed the JRI portfolio, you had a ~70% chance of each new pick seeing 72% gains, plus another 13% chance at 300%+ peaks.

Which, put another way, means the top 81% of my companies returned an average of nearly 2.5X at their peaks.

Another way to look at it: About 70% of companies I interviewed hit a peak of minimum +40% after my coverage, with 40% being roughly inline with sector and market benchmark returns over that time period.

These returns underscore the inherent volatility of this sector. Swing trading to try to capture that beta is a valid, and arguably critical, approach, especially in this volatile, sideways market.

At the risk of being repetitive, the evidence certainly seems to make it clear: Derisk when you can. The whole resource sector is deeply out of favour currently. Waiting for fair evaluations these days rather than derisking on uptrends means more often than not you’re going to be watching your unrealised gains slip away on you as your portfolio turns red. Don’t fight the trend. Will the bulls behave differently once they finally arrive? Certainly. But now is not that time.

Encouragingly, my Core Portfolio, consisting of companies I have worked most closely with/have higher conviction on (coverage categories 3-5) outperformed my total portfolio by over 30%, handily beating all benchmarks returns by some 20% (even beating gold spot by ~10%). That “second layer” of filters I use to pick my high conviction picks among my portfolio is obviously effective.

It really is a feast or famine industry. Fully 1 in 4 of my picks are currently -65%. And yet, even with that bottom-heavy representation I still managed returns between 44-58%.

3.2.3. Other Musings

I’m not calling out some strict Mendoza line here, but the large majority of losers not recovering after they hit -40% and all winners never breaking below -31% while also having a tendency to keep on winning seems an important data point. There’s a lesson in there. Inertia is real. Fair or unfair, winners tend to keep winning and losers tend to keep losing.

True long approaches in this sector means missing out an huge amounts of beta, so if you plan on never selling ever, you better be extremely selective and extremely effective in those selections.

I need to be more critically discerning, or listen to my inner self a bit more clearly. There are 4 or 5 companies who I will avoid mentioning by name I had reservations about I just couldn’t shake but ultimately opted to work with them.

Unsurprisingly, all of those companies now populate the bottom third of my portfolio. Lesson learned clearly to err on the side of caution. If it isn’t rock solid, it isn’t worth your time. There’s almost 1500 mining companies in Canada. Keep looking.

This is honestly encouraging as it is a clear and easy path to increase my overall portfolio gains by another 10% or 20% or more: Just listen to what my instincts are already telling me. I’m already matching or beating the market. Just tightening up my selection process will produce a materially positive impact.

In a bid to cut this project in half, I will end this part of the conversation here. I will certainly have more data and conversations in part 2. Lots more. In the meantime, I hope I’ve left enough for you to chew on here today.

Look, I feel like I’ve said enough this go round. Look for Part 2 in the next 72 hours where in addition to the company-by-company dissection (I made cards!) I have a section dedicated to reflection on 2024 and looking forward to 2025.

In the meantime, I am off to Vancouver for conference season Monday afternoon, so I need to get this project done and behind me. It took an awful lot of time - honestly approaching four weeks of work.

And while my content pipeline is now backed up a bit again, I do indeed believe this exercise was worth it.

Because this exercise is hard proof - both for me and for anyone reading it - that I am capable of producing not just positive returns, not just sector-matching returns, but actual market-beating returns. And to do so over a 2.5-3 year period I think warrants some recognition. And if I didn’t build it, no one would ever see it.

I am proud of my work, proud of my results, and confident that - having already found a viable path to beat the matket - my selection criteria and knowledge base is only going to continue to grow. Look out 2025. I’m just getting started.

As always, thanks for reading. Drop me a line any time. And keep an eye out for Part 2.

-Matthew from JRI

Endnotes

And if you know this industry you know how much more shady things can get than that.

Kinda like an investing cargo cult - it isn’t about finding the right company, it’s about making the company you work with sound like the right company by saying the right things about it.

Coverage categories 3-5, i.e., companies I work with/like the most.

This one is EV Nickel. Down 60% before a bizarre year-long journey to becoming nearly a 7 bagger best on precious little news. Has since followed a long staircase back down with a new management team.