iTech Minerals 2/2: The Geology

iTech Minerals 2/2: The Geology

Simple, predictable, plentiful - Three hallmarks of successful resource exploration, and iTech has 'em.

tl;dr:

iTech Minerals is midway through a redefining discovery drill program that has them on the path to rerating and market success. Drilling out their Lacroma graphite target has been a strong success and it unofficially keeps getting bigger and bigger. Positive metallurgical characteristics also define what is proving to be a cheap, simple ore body, leading to potentially compelling economics.

What we cover:

i. Land package and development (inc. permitting) ii. What Lacroma is and why it is important to iTech’s exploration thesis iii. How exploration is going at Lacroma iv. Why grade is secondary to other factors v. iTech plans for building more value

Alright, back to iTech. I felt like it was important to take a brief wander over into graphite-at-large in my previous post as it provides important context for when we circle back to chat about ITM’s geological thesis. Which is right now. So welcome to my part 2/2 introduction to iTech Minerals (ITM.AX).

Again, quickly, if you don’t have a trading account that lets you buy international stocks, get one – the ASX especially has lots of very strong resource plays. London seems more iffy these days, at least in my opinion. Anyway. Point is, get a brokerage account that does this for you. Again, I have really liked Interactive Brokers.

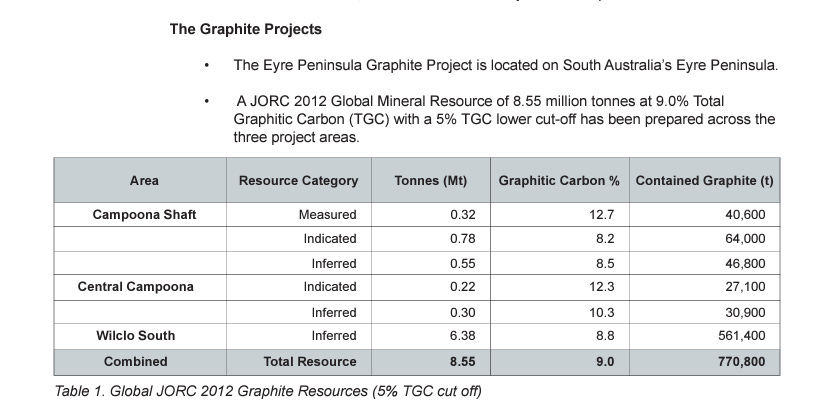

So in part 1, I talked about all the above-ground advantages iTech offers. However, the plain and simple truth is that iTech is achieving critical success through the drill bit as you are reading this. They are ~2/3 of the way through a 10,000M program that is demonstrating strong indications of economic viability. The drills are hitting strong assays where they thought they would, hitting the grades they thought they would, and are uncovering additional targets. Metallurgy brings other good news, confirming Lacroma’s simplicity and suitability for concentration and spheroidization refinement. While Sugarloaf, Campoona, and other targets are also part of iTech’s portfolio, their flagship target - and core focus of this discussion - remains Lacroma.

i. Land Package - the Benefits of Permitting

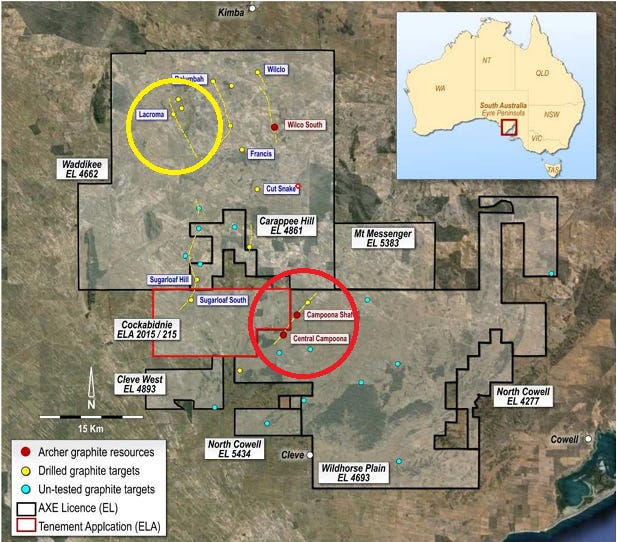

So, to begin with, this isn’t unexplored land. People have known graphite was in the ground here for a long time. Modern attempts at exploitation saw a company called Archer Minerals drill out a number of prospects in the land package and conduct extensive metallurgical work to confirm the graphite’s suitability as EV battery anode material – which it was. Indeed, in 2020, Archer actually advanced Campoona toward a PEPR-approved mine plan, meaning it is fully approved for production by the SA government.1

Fast forward to now, and iTech has taken over Archer’s land package and has identified the same opportunity - fine flake graphite that supports spheroidization for use as anode material in electric vehicles. So far so good, but iTech is taking the additional critical step of exploring their land package for additional tonnage that meets these needs. And this explains their focus on exploring Lacroma.

ii. Lacroma and its Significance

And how goes that exploration? Put simply? Pretty darn good. Lacroma consists of a series of parallel “fingers” of orebody that run roughly parallel to surface but dipping gently. Some make contact right at surface, while some descend up to 200m below ground. Regardless, is that iTech is right smack in the middle of some pretty important derisking events:

Proving that their geological thesis based on EM survey anomalies works;

Identifying and proving up further, unexplored, targets based on those anomalies; and

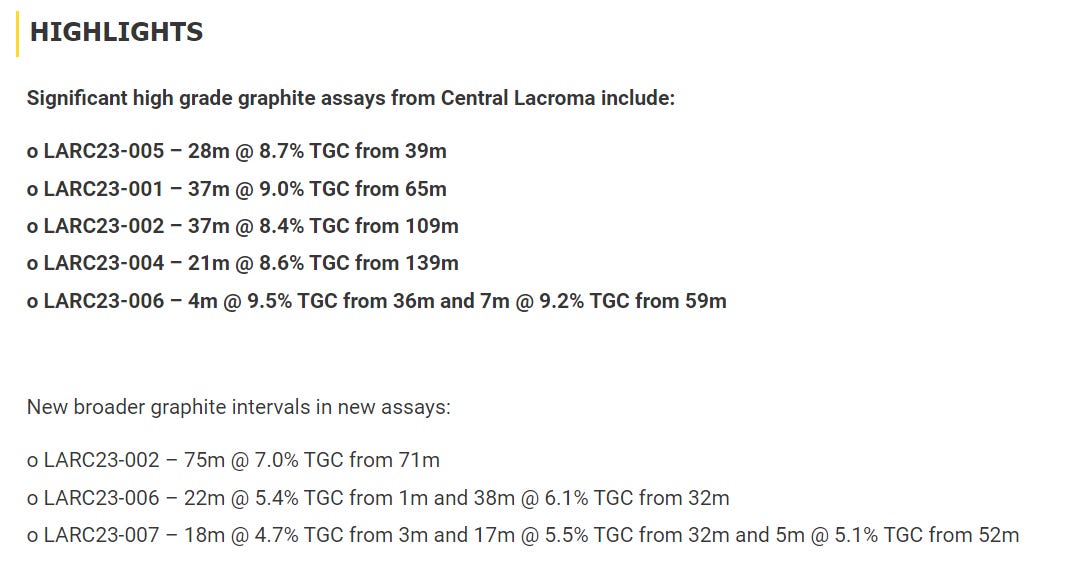

Discovering that these anomalies consist of long, clean, consistent intercepts of (likely - need a JORC-compliant resource of course) economic assays. Take a look at some here below:

Proving that Lacroma ore is metallurgically similar to Campoona ore and can be fed through the PEPR-approved Campoona milling process (again - very cost effective additional tonnage) at comparable recovery rates.2 This is a critical detail

iii. Exploration at Lacroma

Positively, drilling has meaningfully confirmed and even grown the target that was thought to exist before drilling. Various cross-sections of drill holes have confirmed multiple 100s of meters of strike length, and the lateral, step-out drills look like they potentially have identified a larger, deeper target “finger” west of where they were initially drilling (this partly speculation, and credit to “setfire2thehive”3

Prior to drilling, MD Michael Schwarz stated he hoped to see Lacroma turn into a 30-40mt resource, as that was the minimum tonnage he believed was needed to make this an economically viable deposit. Based on initial results, there is a very good chance the final tally could be significantly larger.

iv. Why Grade Doesn’t Matter4

Now, the grades aren’t barn-burners, but for a lot of reasons that isn’t necessarily a huge issue (remember here the graphite primer). Consider:

Clean, consistent, ore - responds positively to simple extraction, concentration, and refinement process.

Close to surface and easy to get to.

Positive tax regime. South Australia has mining-friendly tax rates.

All of these critically combine to make this a very cheap project to get into production, especially considering its advantageous permitted state. These things matter especially in a world with ample sources of graphite. We don’t yet have firm numbers for iTech, but Archer’s plan was very cheap (just $36M in capex) and Lacroma has all the above-mentioned positive traits. These are the sort of attributes you look for in a project, and iTech has them all. They’ve proven their thesis is correct, they’ve proven their ore works metallurgically, and they’ve proven they have more targets.

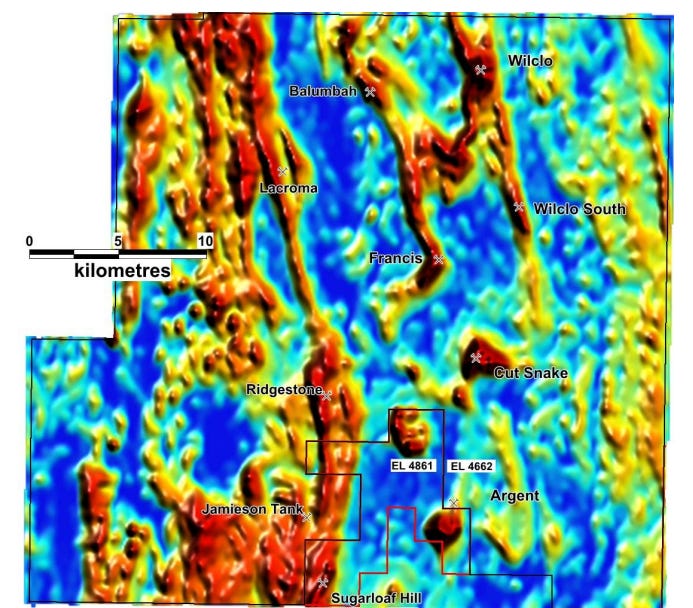

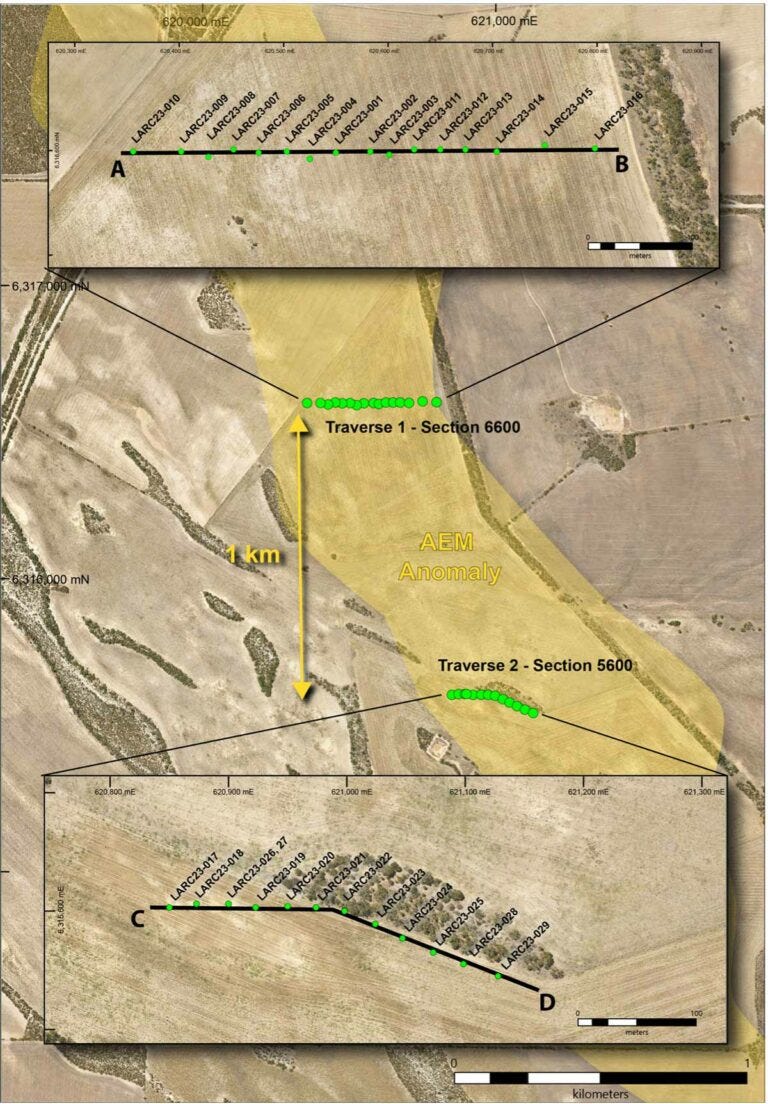

Below is an image from June showcasing the two cross-sections (traverses) iTech had been working on completing at that time. Drill results confirm 2 strong “fingers” of mineralisation according to EM work. That same EM is what makes me speculate the existence of another “finger” to the west.

v. iTech plans to onshore concentration and refinement

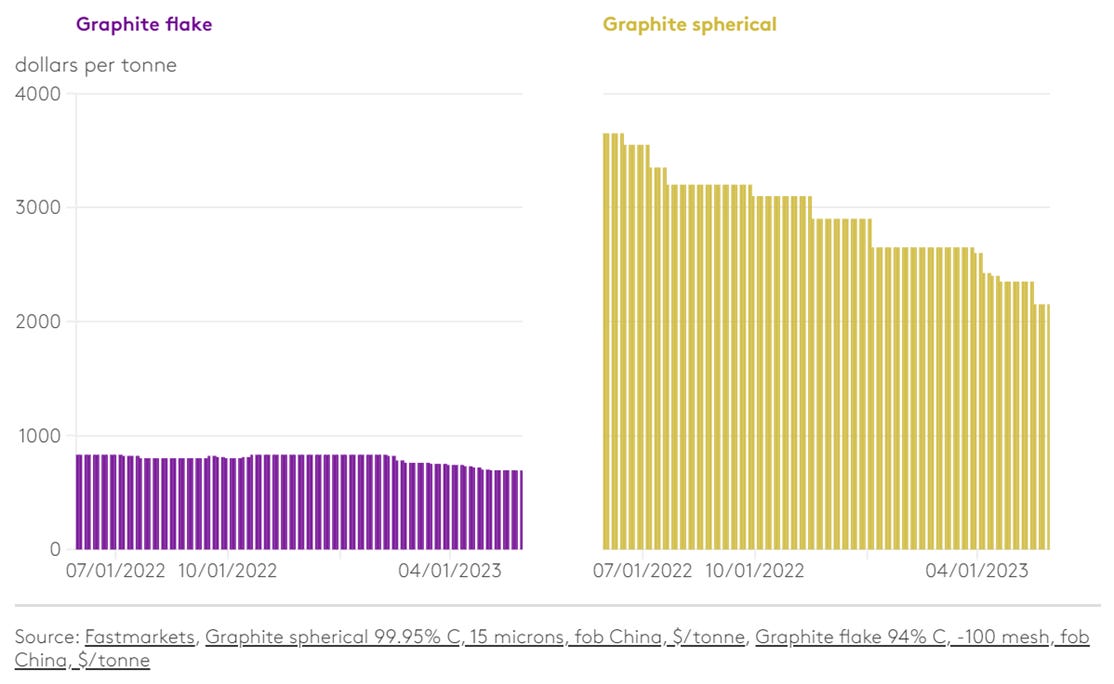

But MD Michael Schwarz has bigger plans than to be another graphite producer living and dying on the whims of Chinese demand and manipulations - he has a vision that includes building a graphite concentrator and a spheroidization refiner to the tune of $300M AUD. This would produce ~50,000 tpa of concentrated graphite, which becomes in turn ~25,000 tpa of spherical graphite worth US $2000-$3000/ton. While the economics are yet to be known, you can start to see the potential for significant cash flow driving a positive valuation, especially in light of the proposed capex which remains modest for the industry and reward. Such a build is no small task, but it is another great example of Schwarz being forward-thinking in his approach and vision.

Conclusion

So there you have it. I tried to keep it simple and efficient, just like iTech’s graphite deposits (har har). I hope I have made my point meaningfully, though. From my vantage, iTech is a great example of a strong company with a strong resource just not getting credit for their derisking works because of the weak macro environment for resource juniors. Regardless, iTech has proven critical things about its geological thesis, keeps adding value through the drill and in the met lab, and keeps building towards a positive outcome for shareholders. And that’s good enough for me.

https://sarigbasis.pir.sa.gov.au/WebtopEw/ws/samref/sarig1/image/DDD/MP453952.pdf

https://www.itechminerals.com.au/investorarticles/drilling-underway-at-the-lacroma-graphite-prospect/

https://hotcopper.com.au/threads/ann-lacroma-drilling-continues-to-deliver-positive-results.7470619/?post_id=68774494

…sort of