Sendero Resources: Drilling into Assays and the Market's Response

MD Michael Wood joins me again to discuss the latest assays from SEND's La Ollita target that showed multiple 100s of meters of mineralisation and reflect on the market's disappointment in them.

tl;dr:

Sendero Resources (SEND.V) has sold off sharply as results from its La Ollita target have been published. Despite multiple 100s of meters of mineralisation, the results clearly now were not enough to please the market. While Sendero’s dream of making the next great porphyry discovery remains geologically very much alive, the tough situation that Sendero-the-stock finds itself in has become the primary story here for the time being. Michael Wood joined me recently to discuss these results and the market response. Below you will see my thoughts on this challenging scenario, as well as the interview and written summary//transcript.

Index

Part 1: The Interview

Part 2: The Companion Article

Part 3: Timestamped Summary and Transcripts

Part 1: The Interview

Part 2: The Companion Article

This is hardly a revelation to people in this game, but the junior resource exploration sector can be incredibly challenging, and even cruel - for both investors and companies. There are so many variables and considerations at play that impact success - prospective geology alone simply isn’t enough.

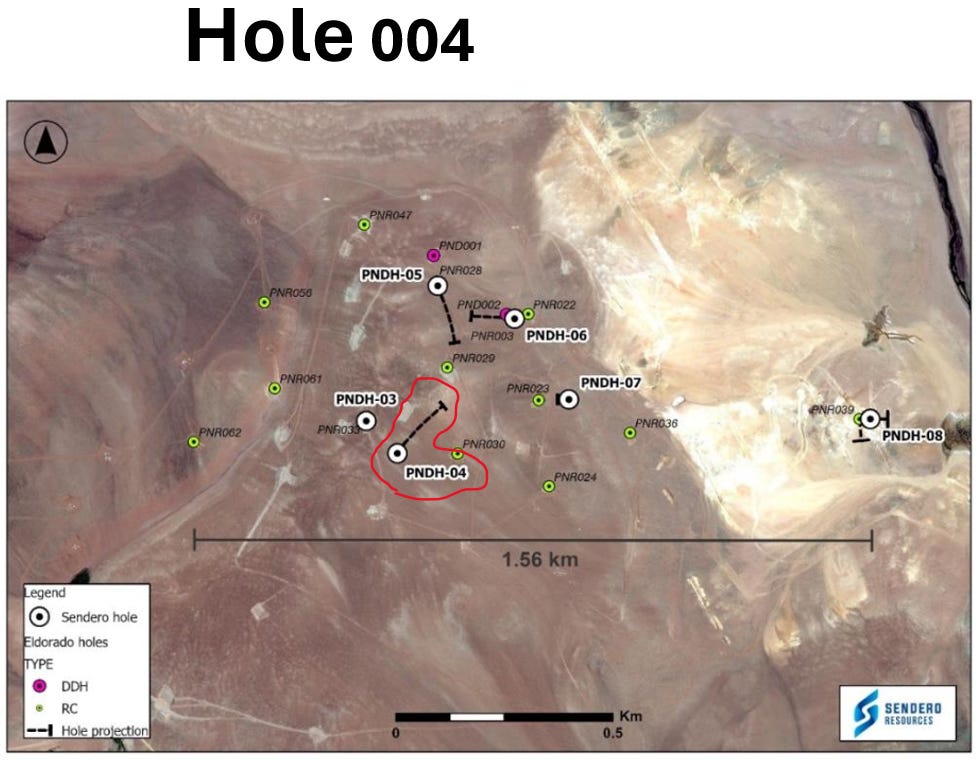

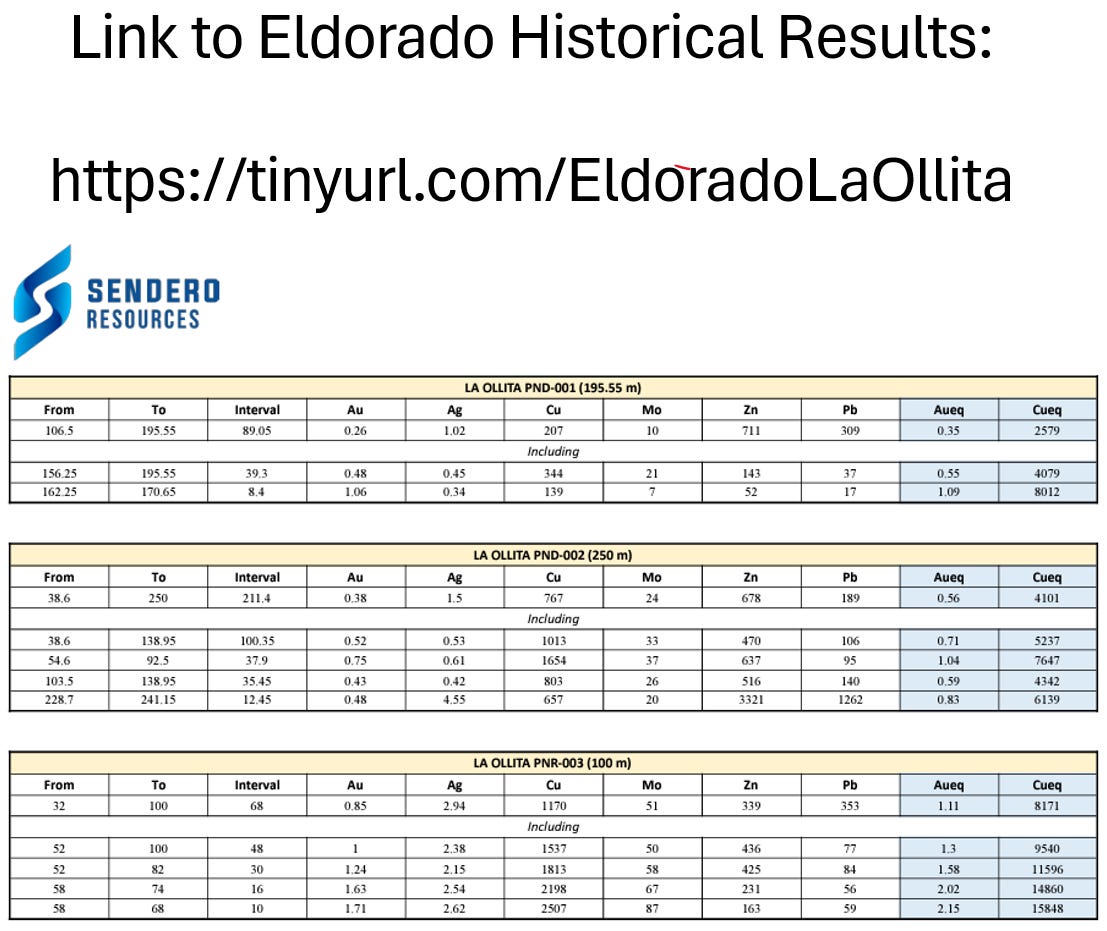

Sendero Resources faces a frustrating scenario presently - they’re currently in the process of receiving assays back presently for their La Ollita porphyry target. With 4 holes back from the lab, the results have been not too bad, and actually quite good if you consider it’s the first 4 holes drilled into the system in nearly 30 years. Take a look:

PNDH003: 256M of 0.53 gpt AuEq

PNDH004: 266M of 0.52 gpt AuEq

PNDH005: 300M of 0.36 gpt AuEq

PNDH006: 364M of 0.51 gpt AuEq

Now, for full transparency, that AuEq is a combination of a number of different metals (though above cut-off grades for the district), true widths are unknown (though you can safely assume they will be lengthy considering the nature of the system) and recovery is assumed to be 100% (neighbours consider recoveries around 80%).

Now, are those candidates for “hole of the year”? Certainly not. But - assuming scale can be achieved - those certainly appear to be economic grades and would be considered as such by their much more advanced neighbours like Filo or NGEx. So, like I say, not too bad. And for the first 4 modern holes into the system I would even go so far to say that they’re pretty darn good. Lots of strong projects have gotten off to much weaker starts than 250-350M of ~0.5 gpt AuEq. Even more, that ~0.5 gpt over multiples 100s of meters mark fits within what I would have considered a success pre-results.

And yet, Sendero’s share price is down - big time. After hovering around 40 cents for the first few months of 2024, Sendero is down some 75% to just 10 cents now post results.

I like to think generally I am pretty tuned into anticipating market responses and understanding the “why” behind how the market moves but this one honestly flummoxes me a bit, in particular because my thoughts continue to be that those results are not bad. And yet here we are, me wrong and apparently with egg on my face, and the market in the middle of a huge sell off as if Sendero’s results were some sort of unmitigated disaster. So why? What’s happened to prompt this?

My thoughts on the “why” are as follows:

Heightened or unrealistic expectations.

A failure to develop the project further than Eldorado did in the mid 1990s.

Expecting copper and getting a gold-dominant system.

Sendero needs to raise money so it’s getting held hostage in anticipation.

The market knows Sendero won’t be drilling again for at least 6 months.

My gut tells me that all of these played a role, but that ultimately the last two points - the need for money and the time before more drilling - is weighing the share price down the most. The results being “good not great” has failed to spark enough demand to overcome the market’s propensity to head for the exits when explorers need money and have no further catalysts incoming. So despite the fact that Sendero has largely done what it set out to do, it finds itself in an extremely difficult position.

Like I said, this sector can be extremely difficult and cruel to navigate.

Because there is a high-grade, company-defining feeder zone lurking beneath La Ollita somewhere, waiting to be found. A feeder zone that could produce the kinds of assays the market is maybe waiting to see - the kind of assays that cause those dramatic rerates investors dream of when they enter this sector.

But it is going to take time, money, and meters to find that zone. And with this sort of market response, suddenly you can’t help but wonder if Sendero will be able to raise the capital required to make that discovery. And if they do, you worry about the levels of dilution required to make it happen.

The potential prize remains intact, but the belief in Sendero’s ability to deliver it to market has been impacted. It certainly isn’t fair, and seems cruel that Sendero is in this position after generally delivering what it had stated its goals to be, but that’s my whole point. This sector is challenging as hell, and what is “fair” often doesn’t really factor into outcomes.

It can of course be particularly frustrating - La Ollita could very well still become the next big Vicuna discovery. So Sendero could very well end up “right” and be vindicated. But if they don’t make that discovery themselves, then even if they are right, they won’t have succeeded as an investment. Welcome to junior resource investing.

So while the quest for the feeder zone will be its own challenge, it is no longer the biggest risk facing Sendero in my eyes. Rather, geology now takes a backseat to the boardroom, as financing and dilution are the most immediate risks facing the company. MD Michael Wood referenced in my interview as well as his recent interview with the KE Report a hope to be able to secure some non-dilutive financing. And for the sake of SEND investors, you certainly hope he manages it. Getting a strategic investor or some sort of JV signed would be the legitimizing shot in the arm this project needs to course-correct a bit.

I continue to watch this play closely, and I am certainly rooting for it still. You want the junior sector to swing for the fences in a way Sendero has done, rather than repackaging the same tired, old parcels of land. And the geological thesis certainly appears to be very much intact. There’s just that pesky, all-encompassing question of financing the dream that needs to be dealt with first.

Part 3: Timestamped Summary and Transcripts

Timestamps are links to that moment in the interview.

01:00 Overview of Results

Michael explains the drilling results from La Ollita, focusing on the geological implications of their findings within a lithocap environment. He notes the continuous, although not high-grade, mineralization across significant intercepts, with some results showing promising silver, lead, and zinc content due to intermediate sulfidation veining.

05:00 Lithocap Model and further exploration

Looking forward, Michael talks about the next steps in exploration, emphasizing the need to locate the feeder zones associated with high-grade mineralization. He mentions historical examples and the strategic importance of understanding the lithocap model to guide future drilling efforts. Michael highlights the geological significance of discovering a large, mineralized lithocap. He discusses the market's tepid response to their findings and the company's plans to secure additional funding for continued exploration.

09:30 Market Response

Michael discusses what he sees as a disconnect between the project's geological success and its market valuation, expressing frustration with the current investor sentiment which doesn't reflect the positive drilling outcomes.

11:00 Mineralisation types and drilling locations

The discussion covers technical details of the drill results, including types of mineralization and geological indicators suggesting proximity to a major porphyry system. Michael gives a detailed account of the drilling process and geological findings, emphasizing the potential of the lithocap environment and the strategic drilling locations chosen based on magnetic anomalies and previous assays.

17:15 Magnetotelluric Survey Discussion

Further exploration strategies are discussed, including the use of deeper geophysical techniques like magneto-telluric surveys to better understand sub-surface structures and guide future drilling towards potential feeder zones.

20:00 Eldorado exploration vs. Sendero

Michael responds to inquiries about the historical drilling by Eldorado and differentiates Sendero's current exploration strategies. He clarifies how advances in geological concepts since the 1990s are shaping their approach. Michael explains how this historical data has helped shape their current exploration strategy and understanding of the geological environment.

26:00 Why is the stock price down so badly

The episode concludes with a discussion about the market's response to the drill results – some combination of hyped retail expectations, the market anticipating a financing, and the end of the drill season. Michael expresses hope that ongoing exploration will eventually showcase the project's true value.

Conclusion

Sendero here underscores for me just how challenging this sector can be at the best of times, much less in a tough bear market as we are now. These results were promising. The chance for a major discovery remains. And yet, were you to hold through results without any derisking, you would be down some 70%-80% right now. I myself am frustrated. I try to be very careful with the companies I work with and I still believe Sendero could deliver good on the immense potential it has in this district. And yet, here we are, down big and the company held hostage for future financings. That being said, if SEND can get financing figured out, I still believe there could be a very bright future ahead for it.

Thanks for reading.

-Matthew from JRI