Pricing Premiums: A Deep Dive into the Future of Iron Demand, and the Mont Sorcier Iron Project, Part 1

Cerrado Gold's long-term centerpiece, the Mont Sorcier iron project provides is home to a 1% GMR for Globex. Strong economics makes Mont Sorcier a potential huge win.

tl;dr:

A big one. The original goal was to examine the value - present and future - of Globex’s 1% GMR on the Mont Sorcier Iron project owned by Cerrado Gold in Quebec’s Chibougamau region. The work is particularly relevant as Cerrado recently announced they had officially begun the tender process for project financing, led by TD Bank.

The scope of the project expanded rapidly. Valuing the royalty of course in turn meant valuing the project itself, including primarily a stress testing baseline costs and pricing and premium assumptions of the September 2022 PEA. To be able to have a semi-informed opinion, this in turn required some analysis and discussion on future demand dynamics for iron in general, and in particular Mont Sorcier’s high-grade 65% + 0.6% V2O5 concentrate.

So what began as a simpler, project-based analysis became underpinned by a series of more fundamental, macro, datasets and discussions.

This will then be published in multiple parts. Part 1: “A Basic Intro to Mont Sorcier and Globex’s 1% GMR” is found below. It will provide a summary of the project so far. Critical analysis of baseline economic assumptions and future iron forecasting will follow in a part 2, likely at this point after Christmas.

Tickers Mentioned: GMX.TO; CERT.V

Index

The Globex Connection: The 1% GMR

The Team

The History and General Overview

3.1. Location

3.2. Recent Ownership History

3.3. Recent Events

3.4. Exploration History

3.5. Economic Studies

The Resource and Mine Plan

Headline Economics

Next Article: Forward-Looking Discussion on Value

1. Comparison to Champion Iron

2. The Future of Iron Demand

3. Economic Analysis of the Deposit

4. Conclusion

1. The Globex Connection: The 1% GMR

Valuation Scenarios

In July 2020, Globex sold 7 different royalties to Electric Royalties including a 1% Gross Metal Royalty, or GMR, on Mont Sorcier for roughly CAD $1.2m in equities and cash.

That gives us a fairly recent, fairly high-confidence data point on how the market valued Globex’s 1% GMR, at least in 2020. And it doesn’t seem like much.

However, lots has happened since then, as Voyager/Cerrado have continued to materially advance this project and put value on the board, including an updated PEA and improved resource, and are in serious, advanced, talks for financing - an especially critical milestone for huge industrial metal projects.

Below, I have created a chart that demonstrates the value of Globex’s at a variety of price points. I have provided a few different values for consideration:

The simple annual cash value of 1% GMR at a variety of low and high price points.

A simplified NPV8 dcf of the LoM revenue created from the 1% GMR. This assumes Mont Sorcier is 4 years from production, and years 1 and 2 having reduced output as they ramp up.

I have also risked the value at a factor of 0.25. This is somewhat arbitrary, but I wanted to account for the heavy risks inherent to mineral development and production. This is an attempt to build a somewhat realistic approximation of current value.

As you will see, the numbers are robust. Consider the chart and scroll below for my discussion:

These numbers are obviously pretty compelling. If Mont Sorcier ever gets into production, Globex clearly stands to benefit mightily, and also underscores the advantage of investing in royalty companies vs. the underlying project itself. Even prices nearing cyclical lows (as seen in scenario 1) still nets Globex $5.3 million CAD per year, and has a current NPV approaching $36 million CAD.

Assuming the PEA pricing premiums are accurate (more on this in part 2) today’s spot price would result in nearly CAD $11.7 million in annual GMR payments to Globex, which comes with an impressive $78 million NPV. Even risked, this is still nearly $20 million.

Apropos of nothing, Globex’s current market cap is hovering around the $50 million CAD mark. Just saying.

2. The Team

Briefly - Lots of experience and success in bringing resource projects into production in the management team with this project, including iron. Brief relevant notes below:

Cerrado and Voyager executives have significant overlap and a common history - Ascendant Resources.

CEO Mark Brennan has a history of successful forays into developing iron resources, namely with Largo Resources.

In 2006, CEO Mark Brennan announced the acquisition of the Macaras vanadium project in Brazil.

In 2008 he signed an offtake agreeement with Glencore

By 2014, they were in production.

By 2019 Largo was producing over $100mm in cashflow from operations.

Mark successfully raised hundreds of millions of dollars to finance the project.

Went from permits to production in just 3 years.

3. The History and General Overview

3.1. Location

The Mont Sorcier iron project is located in the Chibougamau mining district in central Quebec. Multiple active mines and other exploration and development projects are close by.

3.2. Recent Ownership History

Mont Sorcier has been sold a few times before settling into its now-longterm owners Voyager/Cerrado. Since Globex acquired it in the mid-2000s, this is the ownership history:

2012: Mont Sorcier was spun out of Globex into Chibougamau Independent Mines (CBG.V). Globex’s collection of relevant GMR’s originates here.

2016 was optioned by Vendome (later Vanadium One, later Voyager Metals).

March, 2023: Voyager Metals was acquired by Cerrado Gold (CERT.V) in a non-arms’ lengtrh deal. Cerrado is a smaller gold producer with one active and one near-producing mine in South America, and Voyager remains an active subsidiary with overlapping management. Very roughly, at the time of the announcement, this takeover valued Voyager at about $15m CAD (given the 82%-18% ownership share of Cerrado with former Voyager shareholders post-merger).

Mont Sorcier Land Claims

3.3. Recent Events

The following is an attempt to get you up to speed on the past couple years of relevant news for this project:

May 12, 2021: Vanadium One and Glencore announced Glencore’s support in developing the Mont Sorcier Iron and Vanadium Project. Included in the deal was a $10m financing, an 8 year/100% offtake agreement, further offtakes if Glencore finances project construction, and a right for Vanadium One to claw back 50% of offtake to secure project funding if required.

July 5, 2023: Cerrado Gold Announces Potential UK Export Credit Agency Support for Project Finance at Its Monte Do Carmo and Mont Sorcier Projects. Up to USD $420 funding, or 70% of total project financing.

Oct. 18, 2023: Formal vetting process will not be published until Feasibility Study is completed (given timeline is 6 months).

| 2022 Trade Finance Global Export Finance Hub")

News flow for Mont Sorcier recently is definitely positive. Advancing to the tendering stage is no small feat, and getting 70% of funding in place some time in 2024 is clearly a massive derisking milestone. Sometimes you come across companies and projects that have no hope of ever making it to production. Not so Mont Sorcier.

3.4. Exploration History

Chibougamau is about as brownfield as you can get as a mining region, and Mont Sorcier is not some late-blooming wonder. Rather, it has been known about and explored dating back decades. Some details:

Area is well-explored historically. At least 67 holes were drilled in the 1960s on the North and South Zones in a series of traverses running North-South across the width of the zones.

“Based on its work from 1961 to 1974, Campbell Chibougamau Mines in 1974 generated a grade and tonnage estimate on the magnetite layers within the project area totalling 274.4 Mt grading 29% Fe (172 Mt at 30% Fe for the North Zone, 103 Mt at 27.4% Fe for the South Zone).”

Since optioned from CBG, VONE (now a Cerrado subsidiary) has drilled 5,456m in 28 holes in the South Zone and 20,965m in 59 holes in the North Zone.

Most recent resource (June 2022) has the North Zone at 559.3 mt of 37.7% Fe2O3 Ind. and 470.5 at 34.9% Fe2O3 head grade. (More detail in section 1.3.)

3.5. Economic Studies

A variety of technical reports have been written by the various operators over the years. In terms of economic studies, there have been two published. Basic economics will be covered below in section 1.4.

Voyager has published two separate PEAs - an original in April of 2020 and an updated one from September of 2022.

The updated PEA was done to include various changes aimed at improving the economics - from what and how much is to be mined to how it is to be processed to how much everything costs or is worth.

A Definitive Feasibility Study (no PFS in this case) has been announced since the updated PEA and is expected soon. Indeed, the tendering process for financing cannot happen in earnest until it is released. (Author’s note - skipping a PFS raises an eyebrow, but the updated PEA and the guiding hand of TD Bank’s needs and expectations will likely help ensure the final DFS is accurate and thorough enough to be bankable.)

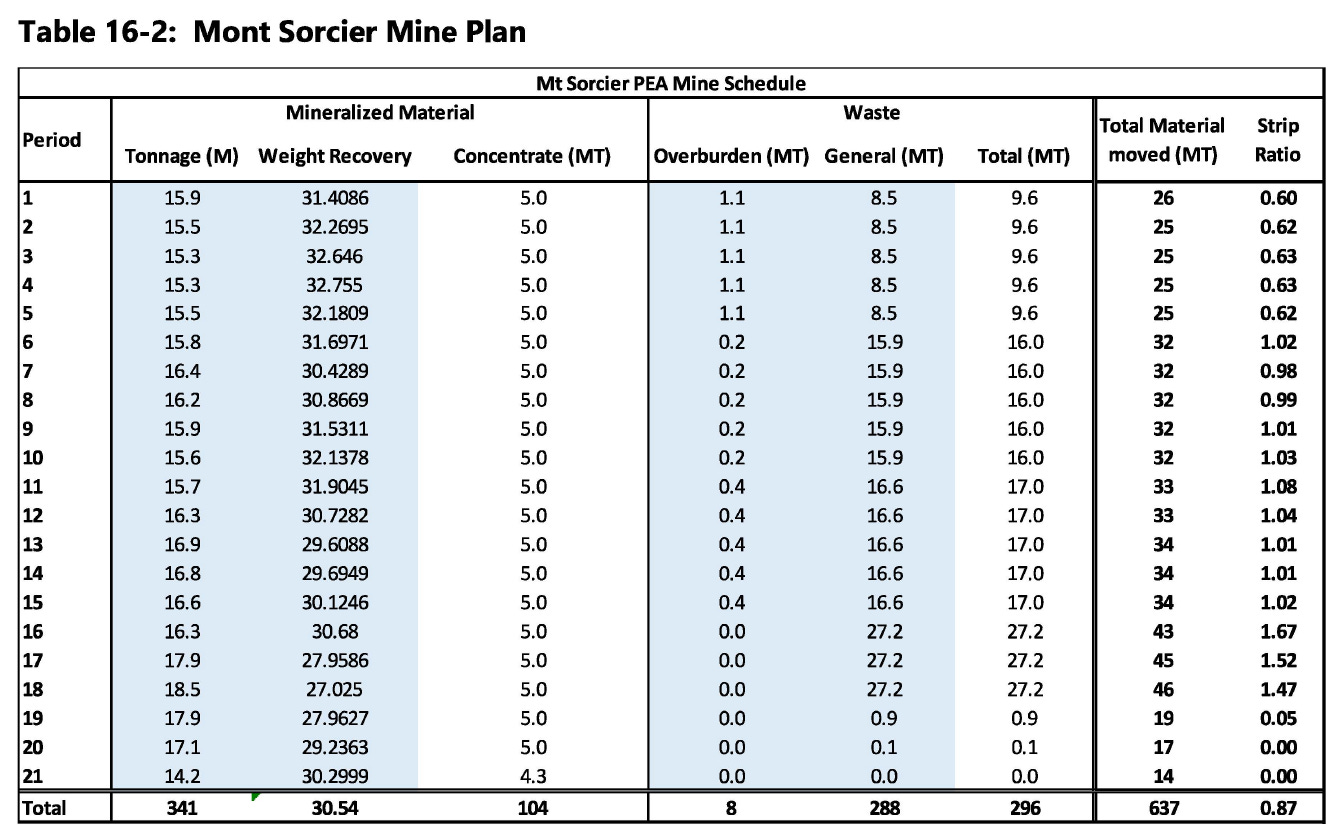

4. The Resource and Mine Plan

Quick Version:

21 year LoM

341.5Mt in current mine plan

There is a "blue sky" opportunity of a further 20 years of production dependent on successful Inferred drilling

16.5Mt of ore to be processed annually

5Mt of concentrate will be produced annually (30% conversion from ore)

Strip Ratio: 0.87 (0.72 if you include the 20.9Mt of inferred counted as waste rock within the preferred pit design.

Produces a high-grade 65.5% concentrate that will command a premium.

High V2O5 content (0.6%) will also command a premium to typical 62.5% pricing.

No penalty elements.

Sulphur is elevated, but can be reduced to within smelter tolerance at 0.1%.

Plans are in discussion to potentially increase annual production to 10Mt or even 15Mt of concentrate.

The Details:

First up, the resource numbers. The simple answer is that Mont Sorcier is, in a vacuum, likely big enough and high enough grade to be economic as an open pit operation. 559.3Mt of indicated rock measures up against other Canadian mines. If the inferred can get even 2/3 of the tonnage upgraded, Mont Sorcier has roughly 900Mt of ore in the North Zone alone, more than enough to produce those multigenerational mine lives you want to see from your iron projects (working from the PEA’s assumed 16.5Mt of annual ore being mined to produce 5Mt of concentrate). Here’s the breakdown of the tonnage:

However, there are some wrinkles that make the current mine plan not account for the outright majority of the tons above.

First off, the South Zone is out entirely. Smaller, adds another pit, and was deemed unnecessary for current planned operations. But that isn’t the end of it. Rather, the preferred mine plan currently only mines out 341.5Mt from the North Zone alone, focusing entirely on the area that has been upgraded to indicated.

Of course, the confidence levels of these massive bulk tonnage operations is higher than, say, a veiny gold system. So you can likely reasonably believe that most of the inferred will be converted at roughly similar tonnage and grade. However, you still have to drill to convert those tons, and to my knowledge this is not in the current plans. So 341.5Mt is what is being brought to market for potential suitors (along with whatever implicit value they choose to attach to the inferred tonnage). So the 21 year mine life is inherently conservative in nature.

However, despite their exclusion from the mine plan, both the North and South Zones in their entirety had their resources pit-optimised, and land required for their exploitation was set aside in the current mine plan. So while Voyager/Cerrado opt to move forward with the smaller version of their project, it is obvious they expect both to ultimately be considered mineable. See the image below for the pit shells, noting the yellow section of indicated resource in the larger North Zone that serves as the current preferred mine plan.

So ultimately you have this strong, high-grade product, valuable high-grade kicker, less than half of the (well understood) resource in the existing mine plan, low strip ratio, opportunities for improvement, no penalty elements, etc. All this to say: These are good rocks conducive to economic mining.

5. The Headline Economics

Finally we’ve got to the fun part. I want to stress here I will be simply relaying numbers from the PEA for now. My dissection will wait for part 2. That being said, this is one heck of an economic project. Consider:

From 2022 PEA:

These numbers are extremely strong. Post-Tax NPV to Initial Capital Ratio is excellent, especially for a large mine. So too are the IRR and payback numbers. Free cash flow annually in the base case scenario is an eye-catching US $235 million.

The base case (see below) iron prices used are not outlandishly optimistic, but neither are they overly conservative. Consider that the NPV rises and falls US $320 million with every 10% change in the iron price, meaning the NPV for Mont Sorcier approaches zero at around US $67.50/ton. Iron prices have been very volatile and there is a debate over the future of iron demand. Stress testing these assumptions with a more bearish analyses interpretations will be a goal of mine with part 2. It is easy to make money when times are good. It is when times are bad that ultimately separate a producing mine from a care and maintenance mine.

In other areas, as you can also see above, the PEA makes two critical assumptions regarding the impact their high grade concentrate and V2O5 kicker will have on pricing. Those two premiums are real and will no doubt benefit Mont Sorcier’s economics greatly, but I will also be looking into them in more detail in part 2 of this project. Understanding their upside -and downside - potential is a critical part of understanding Mont Sorcier.

As for costs, here is a breakdown from the same PEA:

The numbers again are compelling. However, again, though, I will be troubling them a bit in part 2. I believe that operating iron mines in Quebec offer a fair data point in comparison and contrast to these PEA numbers. Luckily, while lived AISC in this inflationary era has proven to be higher than Mont Sorcier’s model, the project itself still will likely manage to remain economic in all but the hardest of pricing down turns. But more on that later.

As for Globex, well, I believe this project underlies the true power of investing in royalty companies. Jack Stoch loves his GMR, and you can see why. No development or dilutive risk. No fear of a falling price. Just a clean and simple money tap that gets turned on when production starts.

Conclusion

Ultimately, Mont Sorcier looks to be a heck of a compelling project. You have a management team that has turned a junior explore co into an iron producer before. You have a large, robust deposit with clear potential to double or more, and will command price premiums. You have a world-class jurisdiction that already is home to multiple iron mines. And you have a project that is being materially advanced and not just mothballed potentially just months away from financing being sorted out.

Again, though, this is part 1 of 2. This was meant to be more the summary of the project, where part 2 will be more critical analyses. Iron is a huge market with many variables and a future that is a matter of some dispute. Getting a handle on economic assumptions both good and bad is key, and that will be the core focus of my part 2.

I hope this reads well! It was becoming unwieldly and I have arranged and rearranged multiple times. At this point I need to publish just to make room for one last 2023 interview (Fireweed Metals!). Place contact me if you have any questions! And look out for part 2 sometime between Christmas and the New Year!

Thanks,

-Matthew from JRI

Great article Matthew, GMX have so many potential moon shots but this project looks really promising. Thanks for all your hard work covering GMX and the associated companies.

Great article! I had a look into the Argentine assets of the company in January for an article about the Deseado Massif and its gold-silver deposits. I really struggled to find the (long-term) red flag there but didn't look into the iron ore project.

You've done this - and it looks fairly promising - and this makes the company even more attractrive to me. Seeing the collapse in share rice (I'm in the red massively) makes the wonder. Where is the red flag with this company? They have a market cap around 30 million CAD.

Looking forward to part 2!