Patience Pays: Waiting for Value to be Recognised (GMX.T)

Globex provides an asymmetrical risk:reward opportunity for investors looking for strong, diversified exposure to commodities.

tl;dr:

Globex is a smartly-run company with a huge variety of projects in its portfolio trading at a deep discount to its intrinsic value. Patient investors will have a great opportunity at powerful returns by buying into this “mini-ETF”.

Globex Mining Enterprises (GMX.T, GLBXF, G1MN) is another intriguing name you should know if you’re trying to make this sector your home. Globex sits in its own little corner of the market. In part an explorer, developer, producer, project generator, and royalty company, CEO Jack Stoch has built GMX into a unique vehicle for investors, serving almost as a sort of unofficial ETF for investors seeking exposure to a diverse range of junior resource projects.

Our interview covered a lot of important ground – Jack’s managing philosophy, plans with their war chest, the future of Globex, and some project-specific updates. It will be more introductory in nature but hopefully there will be value still for pre-existing investors. Go take a look at my interview below, but in the meantime I thought I would share a few other reasons I like Globex:

1. Preservation of Investor Capital: Jack defends his company float tenaciously. Since going public in 1987, Globex has grown to a grand total, pro forma, share count of just 57.7 million shares, with no stock rollbacks ever. That is obviously effectively unprecedented in the sector and has a number of knockdown effects. With traditional juniors, the need for further financing – and thus dilution – is eternal. Long-term investing in this sector means your capital will always erode over time. If anyone has watched a company get caught in the dilution death spiral they will know why this is such an important point. Globex, in contrast, offers no such risk. Globex provides a unique opportunity at longterm investing in this sector without chronic value destruction.

2. Diversification. Another critical advantage Globex offers is the built-in diversification they offer. 232 projects. Scores of different minerals. Everything from gold and silver to lithium and nickel to talc and sodium sulphate. Gaining a deep understanding of even just a few metal sectors can take years, and limited knowledge means inferior investing. Globex offers you exposure to a staggering number of projects with legitimate value assessed and selected by Jack and a small team of geologists and experts. This big basket “ETF experience” of course provides value and exposure impossible to replicate on your own.

3. Revenues and Royalties. The portfolio of projects and royalties that Globex has developed provides access to revenue in multiple ways.

a. One is through the royalties Jack has slowly built up over the years that are slowly turning into revenue streams. Jack figures that anywhere from 1-3 projects will produce revenue for Globex this year. This also obviously further encourages the sort of stable, long-term view of value creation as does Jack’s protection of the company float.

b. Another revenue source is the outright sale of assets. Jack has had a few big successes on this front the past couple years, converting 3 assets via sales to Emperor Metals, Yamana Gold (now Agnico Eagle), and Electric Royalties into roughly $40M in cash and $10M in share payments over the next few years. This naturally raises the question of what could be done with this large influx of purchasing power.

With 90 royalties, even a conservative outlook sees revenues potentially scaling strongly over a multi-year period as projects start to come online and/or be bought out. And there’s the strength of Globex - where there is only one path to shareholder value creation in a traditional explorer – that is to say a discovery - Globex plays the game from a wide variety of angles and provides multiple opportunities for a win while simultaneously protecting against downside in important ways.

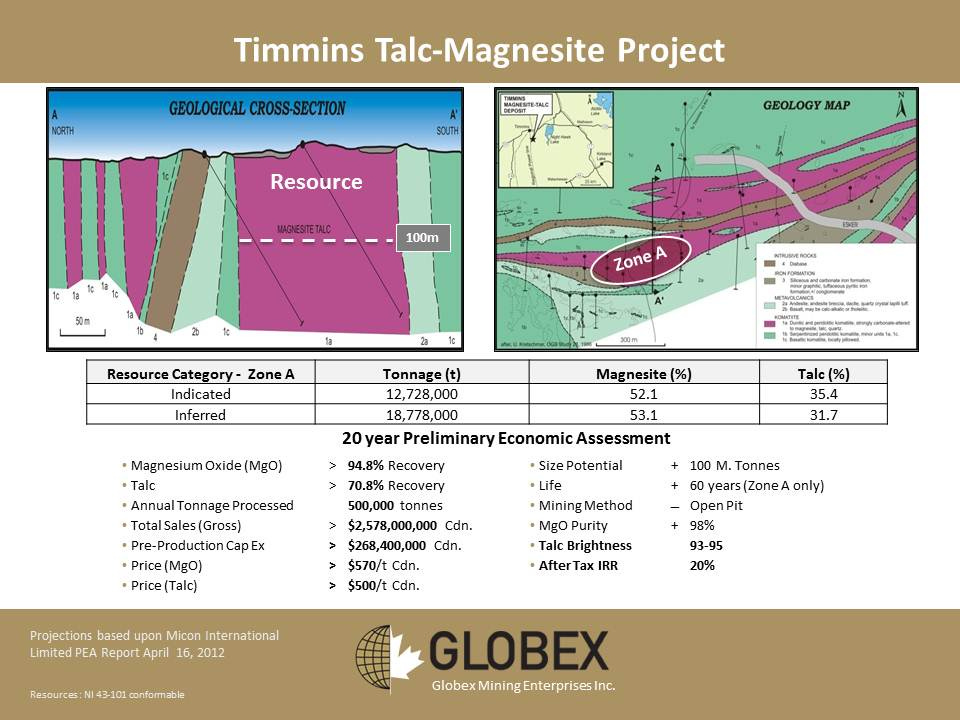

4. Trading at a Deep Discount. Look, every junior under the sun is touting that it is undervalued these days. And honestly, lots of them are probably right. But, boy, if Globex isn’t on a different level. There’s a couple examples I think that nicely highlight what I am talking about. First off, their Timmins Talc Magnesite project has an NPV attached to it that alone could justify Globex’s current market cap. Another example I like is that in the past 2 years, Globex has managed to sell a small handful of its projects for cash and shares that collectively exceed their current market cap. Not sure how much more obvious it can get things are very, very cheap here. Ultimately, if Jack were to decide to sell every project he has in his portfolio, he would undoubtedly end up with returns far exceeding his current market cap. An opportunity at data-driven value investing in the junior sector is, again, a true rarity.

Now, this problem of being undervalued vs. their underlying assets is unfortunately a common curse of the royalty company/project generator company model – anyone with a wide variety of projects tends to struggle to realise the value of all their individual parts. Jack and I discuss in our chat the different factors that might spark a more just valuation in our interview (check time stamps). Here Jack repeats his foundational thesis – it is easy to be patient when you know you’re sitting on asymmetrical value. It might not always happen quickly, but in the end, true value is always recognised. Buying deep value is never a bad idea.

5. Asymmetrical Risk:Reward. Rick Rule has a lot of folksy aphorisms that he gets credit for as a market guru. One that sticks out to me is that if someone offers to remove all your risk for half your reward, you take that deal every single time. That, to me, captures Globex’s story. You won’t get the headline-defining assays and SP bumps and rerates like a New Found Gold or Snowline, but there is remarkably little risk that your capital gets destroyed investing here.

In fact it is quite the opposite - the amount of value available to be purchased at these prices gives me supreme confidence in positive returns from any money I put into Globex, though it may take a bit yet from here for that to occur. Investing is all about stacking the odds in your favour, and to me, for all the reasons above and more, that’s exactly the opportunity Globex offers.

That’s it for me for now. Take a closer look at these guys over at www.globexmining.com. I for one have loved deep diving through some of their many land packages they have up. To conclude, though, this is one of those companies where you could assign a portion of your portfolio to them and walk away, knowing you don’t have to constantly nurse and tend to it like you do so many other explorers. If you buy that the market will eventually wake up – or catch up – to the value story that Globex offers, then all you have to do is buy in and wait for truth to have its day.