iTech Minerals: Update and Interview

I discuss graphite's recent struggles, and have a written interview with MD Michael Schwarz.

tl;dr:

Bit of a surprise update, as I was expecting Mike to take a little bit getting back to me after his vacation. Checking in with iTech Minerals this time with another two parter article. I asked Mike to answer a brief Q and A (which he developed really strong answers to) and thought I would talk graphite a bit ( spoiler: 🪦) as well.

Tickers Mentioned: ITM.AX

Graphite Fall Update External Links:

https://seekingalpha.com/article/4637615-graphite-miners-news-september-2023

https://www.benchmarkminerals.com/price-assessments/natural-graphite/analysis/

Part 1: Graphite

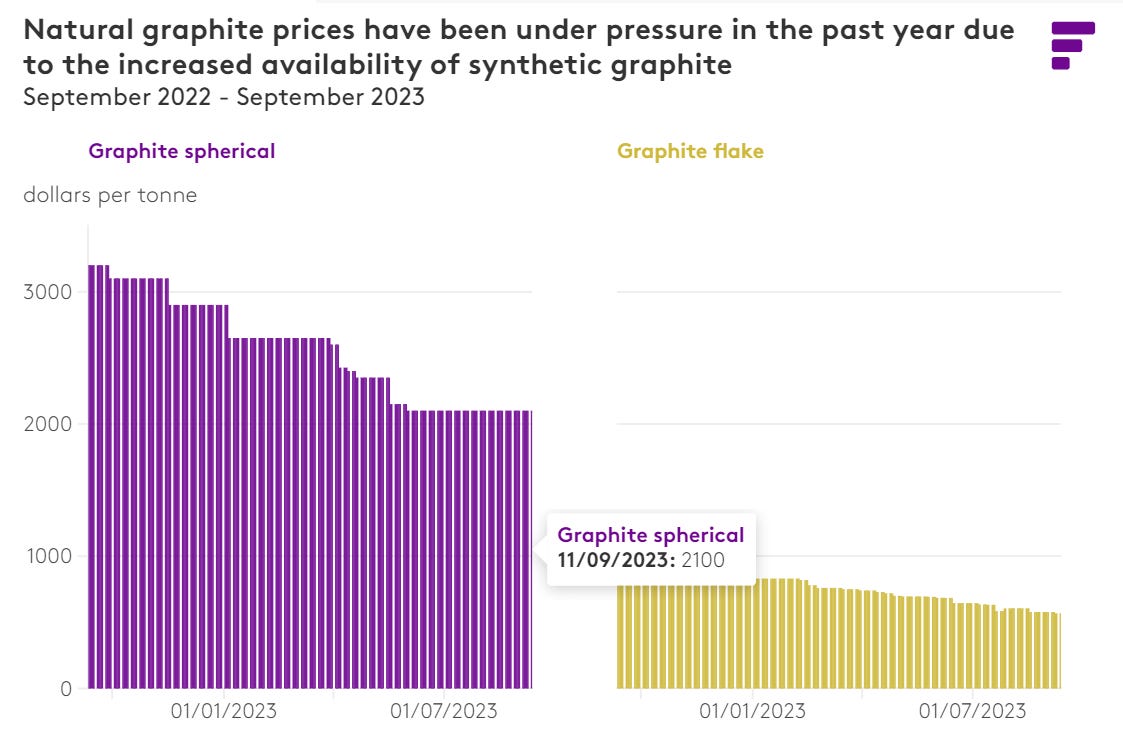

Graphite is in tough. Not really much other way to say it. Prices have been trending down all year. China is overproducing synthetic graphite which is crushing global prices across the board (perhaps underscoring once again the advantages of resource independence for the west). Take a look at the graphs below:

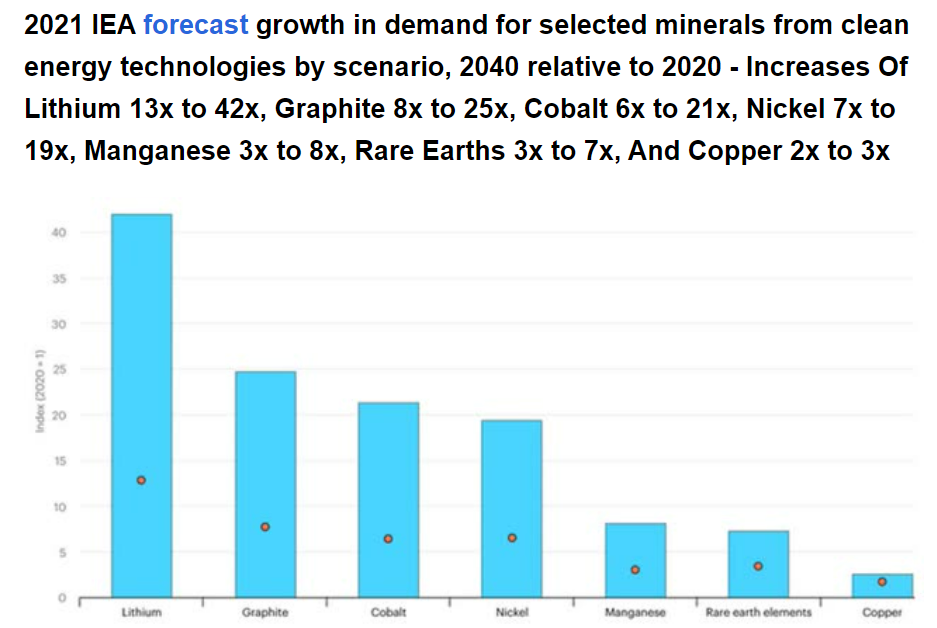

But I find too much focus on short term commodity pricing to be a little too close to navel gazing. There’s just generally not much to be gained by stressing about it too much. This is a cyclical industry. The fact it is down now only means it will cycle back up later. Not to mention there are massive, structural tailwinds starting to build and taking a position in graphite seems like an extremely effective way to take advantage of them. Here’s a graph from the 2021 IEA forecasting growth for various metals. You tell me how meeting demand that is expected to 8-25X in 20 years happens without graphite projects (like iTech’s?) becoming economic and mined out.

So yeah, the graphite sector is kind of facedown in the mud right now. And no, I don’t know where the price of it will be next month. But 2 years? 5? Longer? I have a lot more confidence of where it will be trending over time given the huge forces starting to move about in the background (green energy, resource nationalism etc). So these depressed moments in the resource sector are not the time to run, it is the time to hold on for grim death and remain tuned into the market so you can smartly and slowly and deliberately continue to DCA into companies that align with your thesis and research. At least, that’s what I am doing these days.

Anyway, I don’t want to belabour the point. Read the article links above if you want the full meal deal.

Now, onto the Q&A with Mike:

Part 2: The Q&A

I sent these questions last week and received Mike’s response a few hours ago. They are unedited, but any emphasis is my own.

Question 1

JRI: Where are the drills turning right now?

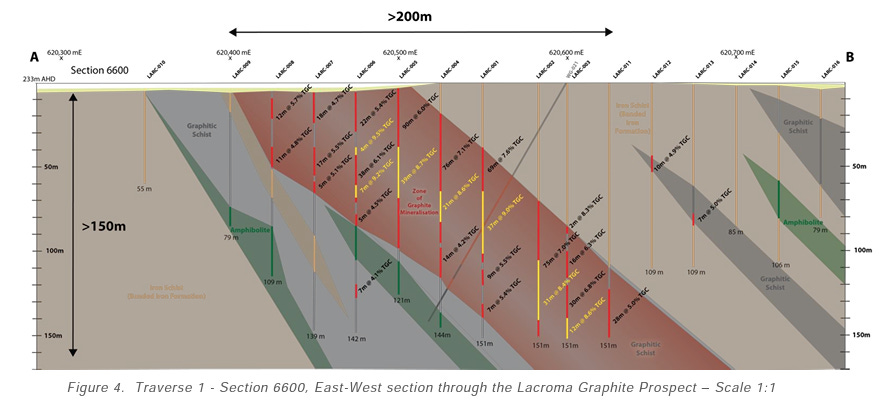

MS: The rig is turning on the Lacroma Central Prospect. We are drilling out the best body of graphite mineralisation within the 4km trend we tested earlier. We are now focusing on a central 1-2km section and drilling this on 100-200m spaced traverses with drill holes spaced 25m apart. We have drilled 105 holes and 11,750m at Lacroma Central with 55 drill holes in the northern half of the resource area.

Question 2

JRI: What is the next major phase of the program?

MS: From now on we are drilling the southern half of the resource area which should be another 50+ holes. This will take us up until the end of the year. Once done, this will drill out a 1-2km strike of mineralisation at a pretty high drill density. I would be hoping for an inferred or better resource to be calculated early in the new year. We will then chase the mineralisation over the full 4km to add extra tonnes to the resource.

Question 3

JRI: What’s the next results planned to come back from the lab?

MS: We have a bunch of assays from the northern half of the resource area ready to go but are waiting on some infill assays to fill out the traverses. These should be back in the next 2 weeks. The next decent batch of assays are due in a month.

Question 4

JRI: Discuss what you’ve proven about Lacroma. Your Before vs Now understanding of it (shape, dimensions, discrete targets, etc.)

MS: We have definite graphite mineralisation over the full 4km of the original target, even though it does thin to ~10m thick at the extreme northern and southern ends. The central resource zone has true thicknesses of up to 70-80m of graphite mineralisation at 6-7% with 20-30m higher grade core of 8-9%. Even though there has been a focus on higher graphite grades in other projects, Lacroma has some unique advantages which should translate to a low cost ore body to mine. Most importantly it appears to be hosted in very weathered material. It is essential clay hosted which means there would be limited if any drill and blast. It would more likely be loader and truck mining direct from the pit. It may even be able to be made into a slurry and pumped out of the pit to the processing plant. Also there in mineralisation from surface and a moderate dip of 45 degrees which is. nice orebody geometry suggesting a low strip ration and pay first from the get go.

With respect to expectations vs what we have learnt now….. I think the main resource zone is thicker and more consistently mineralised than we expected but it does “lense” out or thin more rapidly beyond the central 1-2km. Having said that many other resources around the world have mineralised zones of 10-25m thickness which is what we are seeing outside of the 70-80m zones. I think we were spoilt in the first traverse which raised our expectations beyond the reality that 10-25m could be perfectly mineable given the soft nature of the mineralisation.

The graphite also seems to separate really easily. Even with lower grades of 2-5% we are seeing most of the graphite float on the surface of the sampling buckets which gives the impression of higher grades. I am hoping for good recoveries in the metallurgical test work given what we are seeing.

Our long term target is to add 40Mt and our short term target is to add 20Mt, which is quite achievable given what we are seeing.

Question 5

JRI: What are your thoughts on the Western Anomaly? It’s gotten a bit of a following online - are you excited too or are we misinterpeting the anomaly?

MS: The Western Anomaly.. ahh yes…. It still seems to evade us even though we have now thrown 2 drill rigs at it. What we have found is that there is between 30-60m of transported river gravels and sediments over the top of the anomaly which are very hard to drill through. We have 3-4 decent holes into the anomaly at 100-130m deep and have not identified a source for the anomaly. The host is generally a chlorite schist which can also be the host for graphite but we are not seeing any visual indications. The holes are in for assay but I am not holding my breath. We could have quite easily missed the main graphite horizon but as the drilling was taking up a lot of time and was getting expensive we decided to go back and concentrate on Lacroma Central as this is a much lower risk target to add the resource tonnes we need. It may be that some. So at this stage there are 3 options on what the western anomaly could be. 1. Salty ground water in the overlying river gravels, 2. Manganese mineralisation which was tentatively logged in some holes or 3. Graphite mineralization that was missed in the drilling. I am still holding on to option 3 as the anomaly is much calculated as extending much deeper than the shallow groundwater would produce and the manganese that was logged shouldn’t produce such a strong anomaly. Graphite is till the most plausible answer and we may have just missed it. We aim to go back once the resource drilling is complete and have another go at testing it. Most likely next year.

Question 6

JRI: Reflection on the share price - does it impact your game plan at all? If so, how? And what is your burn rate and cash remaining?

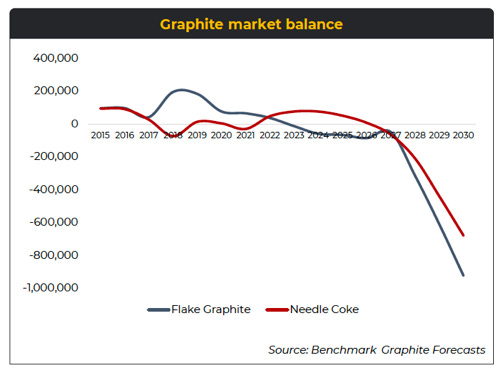

MS: I believe the share price is reflecting the current lower graphite prices for -100 mesh graphite concentrate (my note - see above graph). This is due to a number of factors including the increase in synthetic graphite production due to lower source material and energy costs. This has coincided with a period in China of lower cyclical demand and inventory drawdowns across battery minerals generally, as well as lower prices for synthetic graphite, which has caused increased substitution for natural flake Graphite Concentrates in the Chinese lithium-ion battery anode market. Also in summer the mines in northern China ramp up production of natural flake which leads to increased supply and lower prices. The good news is that we are coming into the winter season in China and these mines shut down and supply decreases. In the past this has lead to significant prices increases. This combined with increasing synthetic graphite cost of production with increase energy and raw material (needle coke from petroleum products) should lead to improved prices in the next few months. I see the current lower prices as a temporary dip in the longer term substantial increase in demand for all types of battery anode material (both natural and synthetic). If the projections are to be believed demand should outstrip supply in the next few years. The electrification of the economy and uptake of electric vehicles certainly doesn’t seem to be slowing down.

Luckily we still have over $AUD5 million in the bank so are not constrained by cash. This should allow us to complete resource drilling, calculate a new resource and finish our metallurgy to get updated economics on the project. We are hoping confirmation of a new resource with supporting metallurgy in a market of rising graphite prices early next year will be a catalysts for increased value in our share price. Given our current price, work underway and cash to complete the targets, I believe we are pretty good value.

And that’s a wrap! Thanks and till next time.

-JRI