Giga Metals: Pre-Feasibility Study Summary

Giga Metals: Pre-Feasibility Study Summary

Economic studies are essential to investor knowledge, but they can be a daunting task. With this update, I read and summarised Giga Metals' PFS - all 440 pages of it - so you don't have to.

tl;dr:

A little bit of a different work today. Rather than making an effort at finding evidence to create an informed opinion, today I am more so summarizing and compiling evidence for you to create your own opinion with. Economic studies and technical reports are such a critical part of this sector, but they can be daunting at times. With this in mind, I did a proper deep dive of Giga’s recent PFS. My hope was to boil down the 440 pages of content into the most meaningful bits to ease your own due diligence process. So rather than analyzing references and data for you, I am hoping I could create my own reference for you to do your own analysis with.

Index:

A Summary of My Summary

Turnagain Project Pre-Feasibility Study: JRI’s Summary

1: A Summary of My Summary

Information from the PFS I think is new, interesting, or important for you to know prior to reading.

Pro tip from my research assistant days: If you have a big document ahead of you and are short on time, just read the intro and conclusion and you will probably get 2/3 of what you need to know out of a document in 1/10 the time. Minus all the great quotes and direct evidence you accumulate from a proper read-through.

All #s in USD unless otherwise stated.

I out of necessity skipped several sections. Not every box plot graph made the cut! Though the spider charts did, because who doesn’t love a good sensitivity analysis?

I have read on social media concerns about this project that it intends to divert the Turnagain River. Which of course is always a large can of worms to open. As someone who believes in environmentally sustainable and best practice mining, this was of course a concern. Thankfully, I learned that the current 30 year mine plan does not include in its resource or open pit design any areas that would require this diversion. This is a good example, I believe, of Giga working in good faith and wishing to be as minimally disruptive as possible with its mine plan. (Also a good example of doing your own research and not relying on the misinformed opinions of others.)

It was quite evident from the read that Giga (and Tetra Tech for that matter) do good science. Exhaustive, iterative, longitudinal studies. Returning to old work to find new and better results. Focusing on shifting from qualitative to quantitative analysis in an effort to produce true geological mastery. If you are as perverse as me and enjoy deep diving into a technical report, this is a good one.

There are numerous ways for economics to be potentially improved in the coming years:

No (minor) Cu credits currently counted;

Sequestration creating carbon credits;

Potential sharing of infrastructure costs with other mines;

Switching to hydrometallurgy;

Repurchasing of an NSR;

Removal of layers of waste rock during mining;

Existence of inferred resources within the current pit design not included in the current economic work

The flow sheet for this mine really is clean and easy. The rocks they’ve selected to extract their minerals from play quite nicely, and mineralization from every part of the deposit responds consistently nicely to the process.

It really deepens my belief that Giga’s Turnagain is a project that will be compelling in the eyes of any major, OEM, or other large JV partner looking for tier 1 nickel in a tier 1 jurisdiction. Turnagain is very forward-facing: Rigorously understood, strong emphasis on minimal GHG and environmental impact, and a focus on stable, predictable, high-quality concentrate. This might not ever reach the valuation multiples of its higher-grade peers, but nor does it need to for it to be a successful investment. Turnagain strikes me as the kind of project that will ultimately become a mine. Which, of course, bodes well for the odds of investment success.

Okay, that’s it for me! Like I say, I try to commit to strong due diligence practices, and I thought this was a good opportunity to maybe pass a gift down to my readers in the form of a summary that is hopefully both authoritative yet efficiently truncated. A reference guide to return to during your own due diligence process.

2: Turnagain Project Pre-Feasibility Study: JRI’s Summary

1.0 Summary

1.2: Project History

Current leadership took over the project in 2004.

After period of dormancy, name changed to Giga Metals in 2017 and company reactivated.

Five historical PEAs have been prepared for the property in 2006, 2008, 2010, 2011, and 2021.

1.3: Geology and Mineralization

Sulphides are mainly pentlandite and pyrrhotite, with minor amounts of chalcopyrite, pyrite, and trace bornite.

Pt and Pd also present and “may be of minor economic interest”.

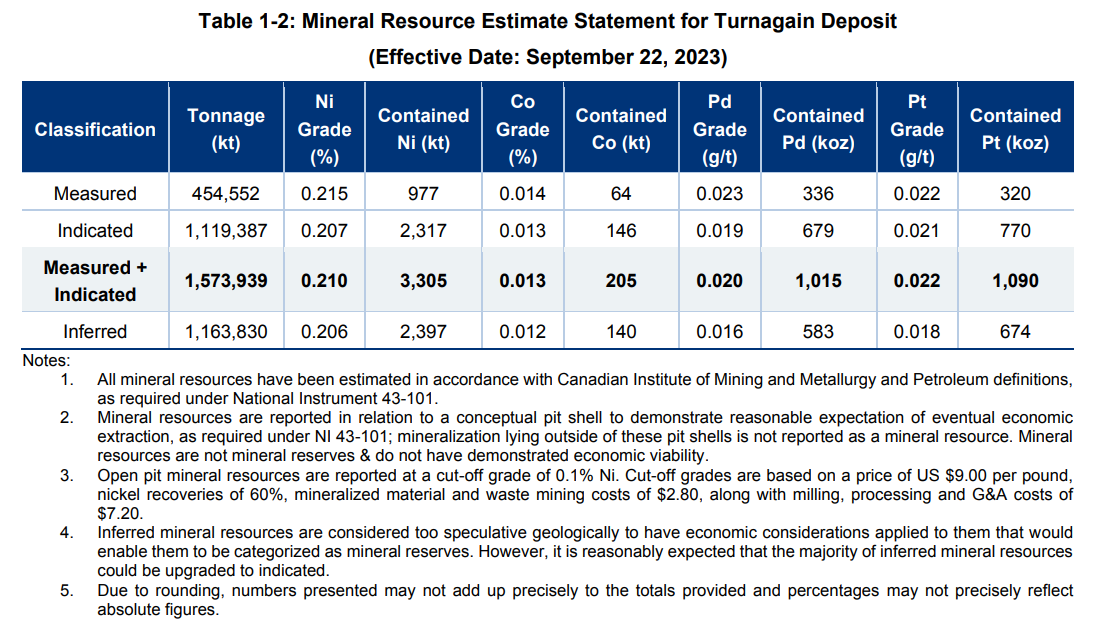

1.4 Mineral Resource Estimate

Cut-off of 0.1% Ni

Contains estimated 1,574Mt of M+I resources at 0.21% Ni and 0.013% Co.

1,164Mt of 0.21% Ni and 0.012% Co classified as inferred.

2.397Mt of contained Ni.

Table 1-2: Mineral Resource Estimate

1.5 Mineral Processing and Metallurgical Testing

Early metallurgical testing focused on hydrometallurgical processing. However, since 2010 work has focused on “the production of saleable concentrates”.

“Turnagain material is hard”, but is an issue readily solved by high-pressured grinding rolls (HPGR)

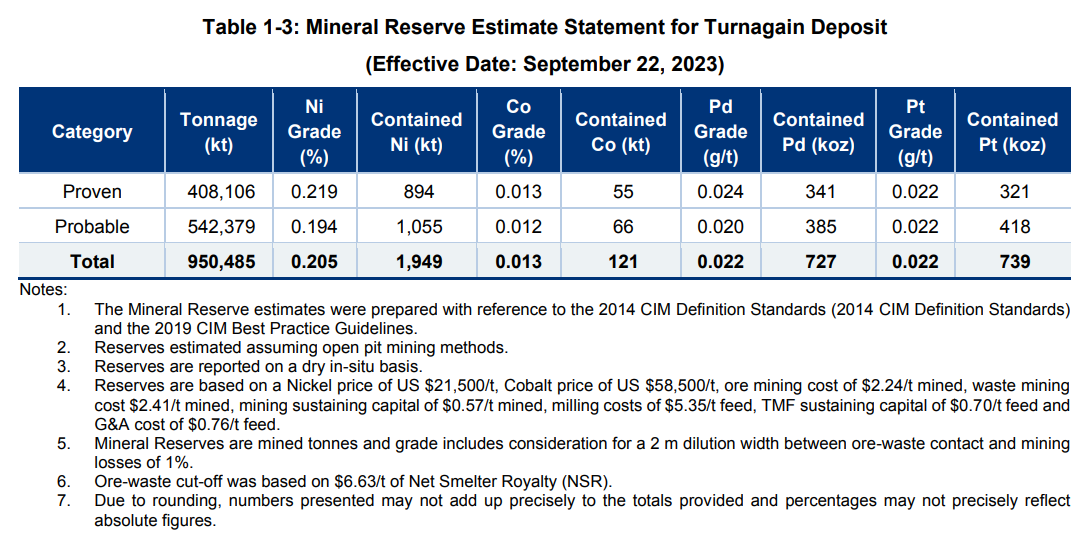

1.6 Mineral Reserve Estimate

~0.950Bt of 0.205% Ni and 0.013% Co.

1.949Mt of contained Ni.

Table 1-3: Mineral Reserve Estimate

1.7 Mining Methods

“Turnagain will be mined using conventional open pit mining methods”

1.8 Recovery Methods

Plant designed for 45,000 tpd in year 1, then increasing to 90,000 tpd for remaining LOM

LOM average mill feed grade is 0.205%

LOM average annual concentrate production will be 196 kt/year

Concentrate grade of roughly 18% Ni.

Peak production to be 237 kt/year

LOM average Nickel recovery of 51.4%

Ore will be crushed twice, then HPGR, then ball mill before multi-stage flotation

1.9 Project Infrastructure

1.9.3 Tailings Management Facility (TMF)

Slurry tailings will be transported by pipeline facilitated through gravity conveyance.

Comprehensive work to meet regulatory and guideline requirements complete.

1.9.4 Overall Site Water Management

Tetra Tech completed flood inundation strategy and concluded a 1 in 200 year flood is unlikely to impact the mining pit.

1.9.5 Power Supply

Requires approximately 160km of 287 kV transmission line to connect to BC Hydro’s Tatogga Substation.

Would require related Tatogga Expansion and new substation at Turnagain.

1.10 Environmental Studies and Permitting

Several Environmental and Social studies are ongoing.

Will require final provincial and federal environmental assessment.

Scope 1 and 2 GHG footprint calculated to be 1.8t CO2 per tonne of Ni.

C02 sequestration studies are ongoing. Results are positive but too preliminary to be included.

Stated goal of Carbon neutrality is believed to be achievable.

1.11 Capital and Operating Costs

Total initial capital cost is estimated at $1.8935B.

LOM sustaining cost is $1.643B, including closure.

+/- 25% as per PFS standards.

Table 1-4: Initial Capital Cost Summary &

Table 1-5: Sustaining Capital Cost Summary

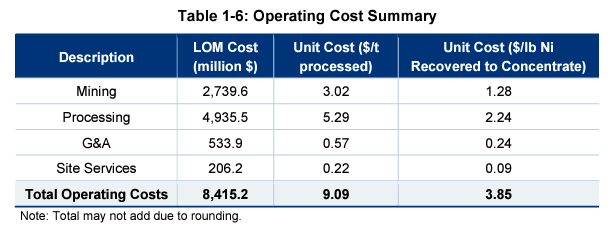

1.11.2 Operating Cost Estimate

Average LOM operating cost estimated at $9.04/t ore processed or $3.89/lb Ni recovered in concentrate.

Table 1-6: Operating Cost Summary

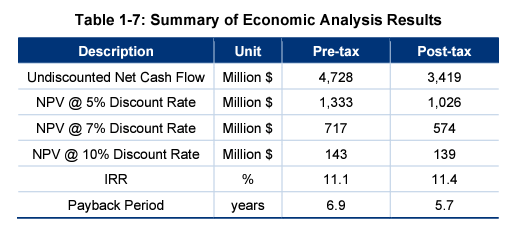

1.12 Financial Analysis

Used a nickel price of $9.75/lb and a cobalt price of $26.54/lb

Annual discount rate of 7% used

Post-tax NPV of $574m

Post-tax NPV of 11.4%

Post-tax payback of 5.7 years

Post-tax IRR is actually higher than pre-tax due to Canadian tax credits

Table 1-6: Summary of Economic Analysis Results

Section 4.0 Property Description and Location

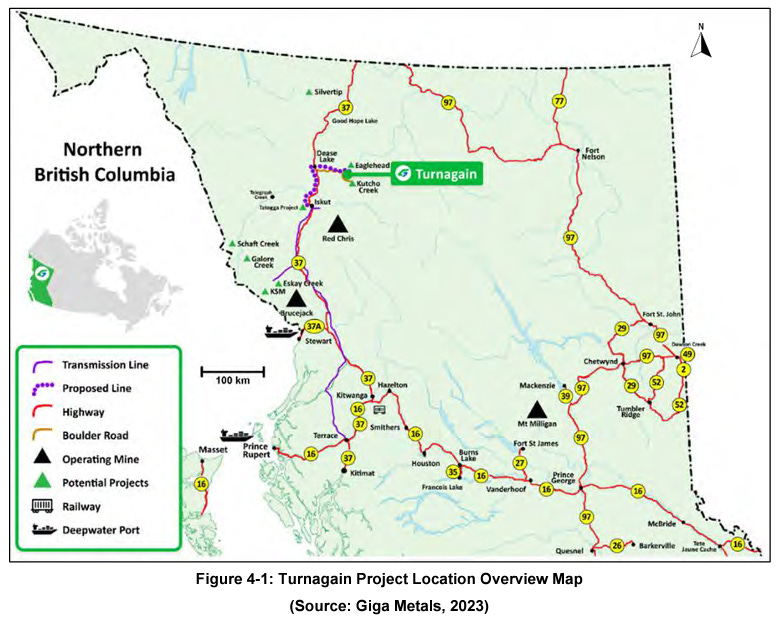

4.1 Location

Figure 4-1: Turnagain Project Location Overview Map

Closest community is Dease Lake (pop. 229).

Traditional territory of the Kaska Dena and the Tahltan.

4.2 Mineral Tenures

Wholly-owned.

75 tenures covering 40,069 ha

4.4 Royalties

Original property vendors retain 4% NSR on a single claim, Giga retains right to repurchase at price of CAD$1m per 1%.

2% NSR held by Conic Metals Corp. 0.5% buy-back availabel for a price of $20M.

5.0 Accessibility, Climate, Local Resources, Infrastructure, and Physiography

5.1 Accessibility

Located 65 km by air from Dease Lake airport (charter hub for larger surrounding communities).

Exploration trail (Boulder Trail) has been consistently used to carry equipment to site.

Boulder Trail has been studied for upgrading to a mining road and deemed suitable.

5.3 Hydrology

Located near the headwaters of the Turnagain River.

Several small creeks flow through or near the Project site.

7.0 Geological Setting and Mineralization

7.3 Mineralization

Semi-massive and massive sulphides identified.

Located within broad zones of disseminated sulphides.

Generally hosted by Dunite and Wehrlite.

Central and Northern Dunite largely devoid of Sulphide minerals. There the highly magnesian olivine contains generally 0.2%-0.3% Ni.

Primary minerals consists of pyrrhotite with lesser pentlandite and minor chalcopyrite.

13.0 Mineral Processing and Metallurgical Testing

13.2.3 Flotation Testing

The baseline PFS flowsheet observed:

Pyrrhotite has proven to be poorly floatable, so pH manipulation is not needed to assist in pyrrhotite rejection, reducing the alkalinity of the flotation.

Silicate mix requires little-to-no talc, meaning gangue floatability is weak, which reduces needs for gangue depressants.

However, silicates can interfere with pentlandite flotation. Balanced use of Calgon assists this.

13.3.4.3 Prediction of Rougher Flotation Recovery

Magnesium, Iron, Nickel and Sulphur (MINS) Approach

Quest for a better recovery algorithm led them to MINS.

13.3.4.4 Prediction of Cleaner Flotation Recovery

Work has been done to understand how poorer-acting minerals would respond to cleaner flotation.

Cleaner flotation response was quite similar irrespective of which zone the project came from.

Advantageous for flowsheet design.

There is potential for development of a hydrometallurgical concentrate treatment route that is more tolerant of Magnesium and may be worthwhile pursuing given the project life, but it was not considered within the confines of the PFS.

14.0 Mineral Resource Estimates

14.1 Introduction

The resource model includes the the southern portions of the Horsetrail zone and the Hatzl zone south of the river.

Exploitation of these zones would require a short diversion of the Turnagain river.

This is technically viable, with permitting precedent, but these zones are not included in current resource statements and are not within the current mine plan.

14.2 Drill Hole Data

382 Drill Holes were in the database

However, only 254 drill holes were used for the purposes of resource estimation.

14.3 Data Analysis

Cu not included in resource estimate but potential in future for it to be.

Table 14-2 Statistics for Nickel

14.4 Geology Model

Lithography denotes relatively flat underlying units.

These have been intruded upon after the fact by late dykes and bounding volcanics.

There exists the potential that these layers of wasteful intrusions could be identified and removed as waste rock during mining to improve head grade of the ore. For now they remain in the mining model and account for internal dilution.

14.9 Block Model Definition

Chosen block size was 15m x 15m x 15m.

Drill holes spaced approximately 50m apart.

3-6 blocks between drill holes.

14.11 Mineral Resource Classification

Typical note that indicated resources at +/- 15-20%, measured at no greater than +/- 15% at 90% confidence.

Hole patterns: Measured requires 3 holes in a 75m pattern

Indicated = 3 holes in a 150m pattern

Inferred = 1 hole within 200m

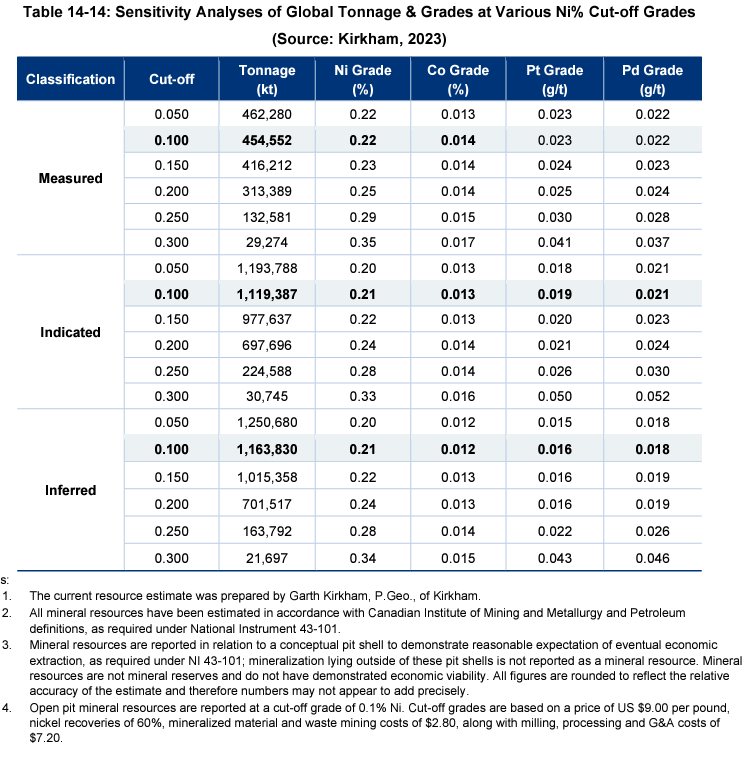

14.13 Sensitivity of the Block Model to Selection Cut-off Grade

Table 14-14: Sensitivity Analyses of Global Tonnage & Grades at Various Ni% Cut-off Grades

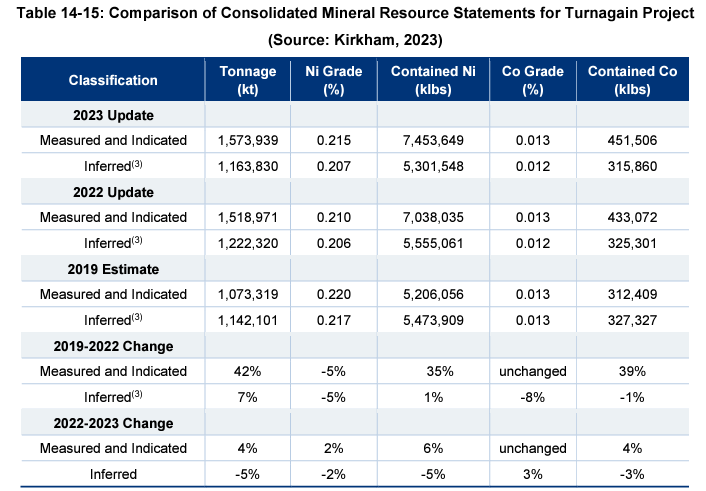

14.16 Comparison to Previous Resource Estimates

Table 14-15 Comparison of Consolidated Mineral Resource Statements for Turnagain Project

16.0 Mining Methods

16.4 Phase Designs

To maximize NPV, 6 total phases to pit development were incorporated to bring higher grade ore forward in the mine plan.

16.8 Mine Production Plan

Optimum mill feed throughput determined to be 32.85Mt/year.

Mining strip ratio averages 0.41 over LOM.

29 years of mining, 2 years of ore feed from the low-grade stockpile.

Figure 16-8: Ore and Waste Mining Schedule

16.9 Mine Operation and Equipment Selection

16.9.3 Hauling Unit Requirements

Trolley-assist technology to be used.

Diesel consumption up to 70% less when in trolley mode.

Speed of traveling up hill is nearly doubled in trolley mode = more productivity, reduced truck requirements, labour, etc.

Trolley-assist trucks expected 25% more engine life.

75,000 gross hours for trolley assist vs. 60,000 regular truck

17.0 Recovery Methods

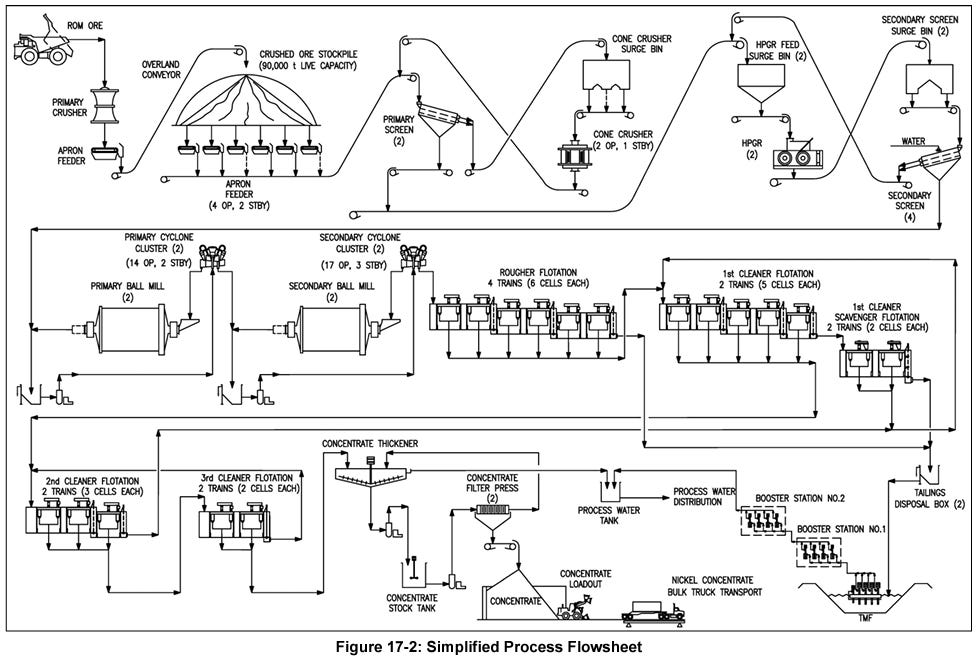

17.2 Flowsheet Development

Figure 17-2: Simplified Process Flowsheet

17.3 Process Design Criteria

Table 17-1: Major Processing Plant Design Criteria: Grades and Production Estimates

17.4 Process Description

Year 1: 45,000 tpd, ramping up to 90,000 tpd for remaining LOM

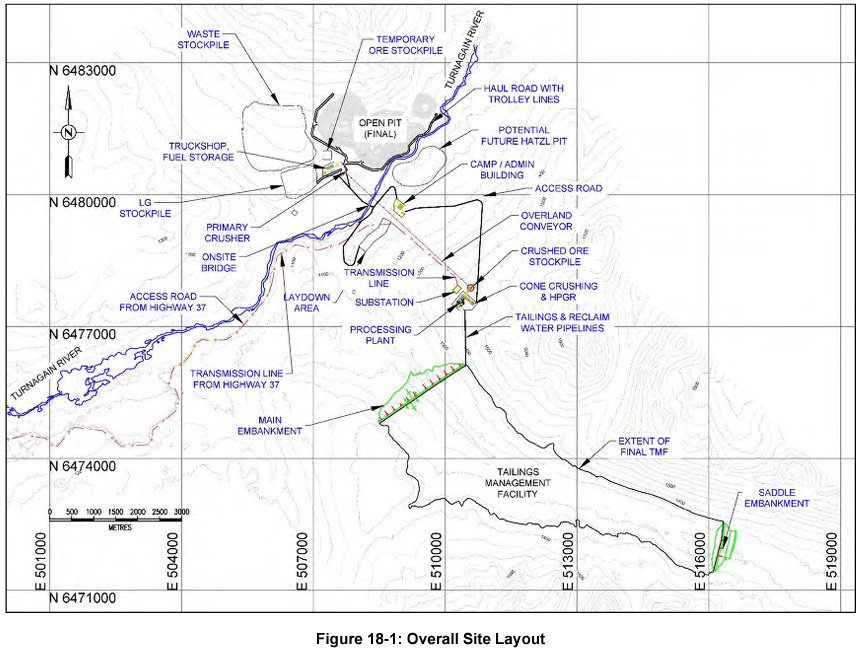

18.0 Project Infrastructure

Figure 18-1: Overall Site Layout

19.0 Market Studies and Contracts

19.1 Overview

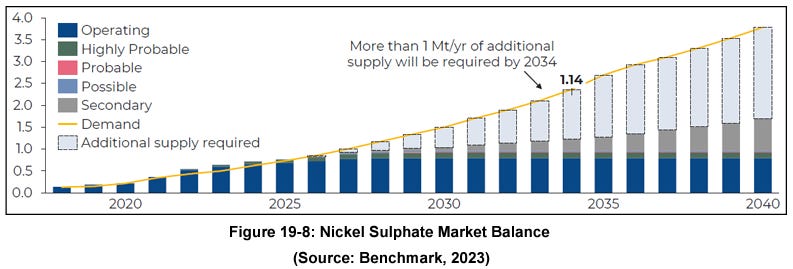

Projected potential 5.3% CAGR for nickel to 2040 (as per Benchmark).

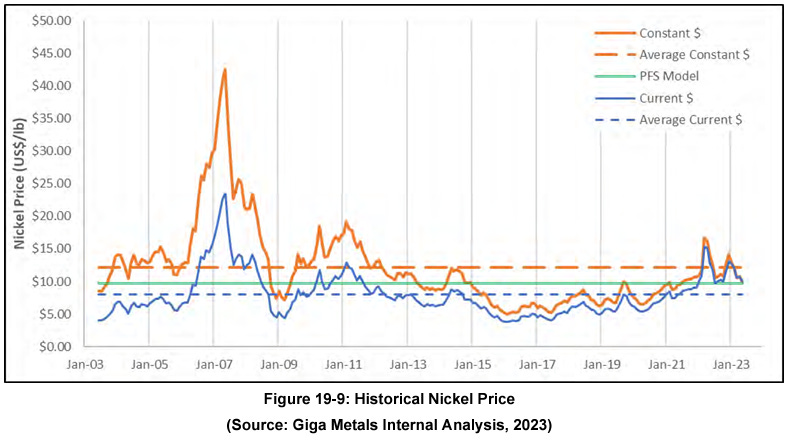

Giga used $21,500/t Ni (19% below 20 year average) as base case.

78% payability of contained nickel in concentrate, net smelting and refining charges.

Cobalt benchmark pricing of $58,500/t “slightly below” 20 year average.

Smelter payability of 50% for Co.

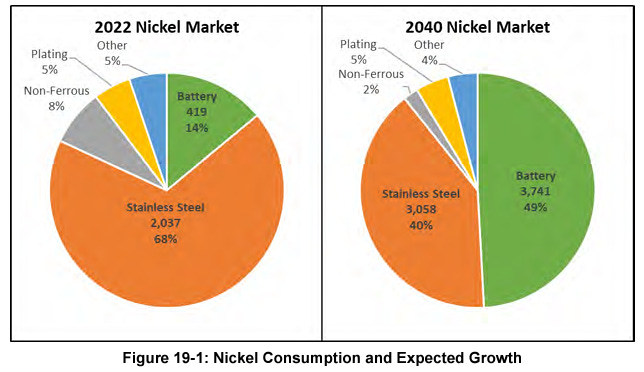

19.2 Nickel Markets - Demand

Figure 19-1: Nickel Consumption and Expected Growth

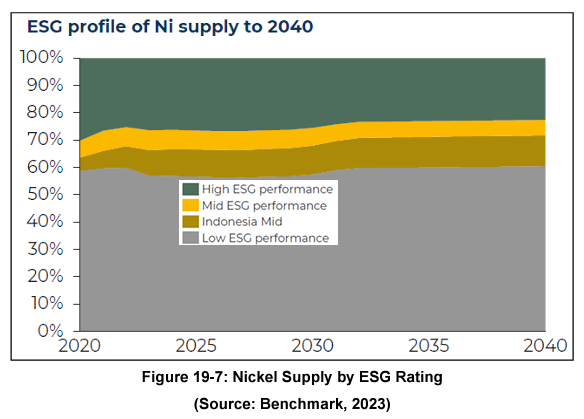

19.3 Nickel Supply

World supply has grown strongly the past 20 years.

Much of recent growth coming from Indonesian Laterite projects.

The expected growth to 2040 is expected to come primarily from Laterite deposits.

ESG characteristics of nickel supply are not expected to improve.

The proportion of the market ranked as high-ESG is actually expected to shrink.

Figure 19-7: Nickel Supply by ESG Rating

Figure 19-8: Nickel Sulphate Market Balance

19.4 Nickel Price

No premium as of yet for North American or high-ESG nickel.

However, Benchmark notes there will be fierce competition incoming for high-ESG nickel during the upswing of the next cycle.

Figure 19-9 Historical Nickel Price

19.7 Concentrate Markets

Global Smelter Terms Review was undertaken for Giga Metals by Benchmark Mineral.

Turnagain nickel sulphide concentrate is high grade. Expected to be in the 75-80% payability range. (78% in PFS.)

Co grade is 1%. This is higher than many other concentrates and should achieve 40-60% payability. (50% in PFS.)

Indicated copper grade of 0.4% - near low end of payability and likely wouldn’t exceed 40%. (N/A.)

PGM grade: Low. Borderline payability. Expect 30-40% payability. (90% after 1g/t deduction.

21.0 Capital and Operating Costs

21.1 Initial Capital Cost Estimate

See Figure 1-4 above.

Expected accuracy is +/-25%.

USD:Canada Currency Exchange Rate of 77 cents

21.1.7 Contingency

Total Project contingency of $177m

22.0 Economic Analysis

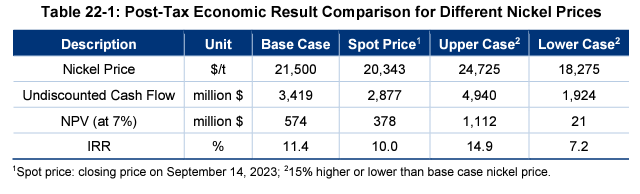

Table 22-1: Post-Tax Economic Result Comparison for Different Nickel Prices

Table 22-2: LOM Production Statistics

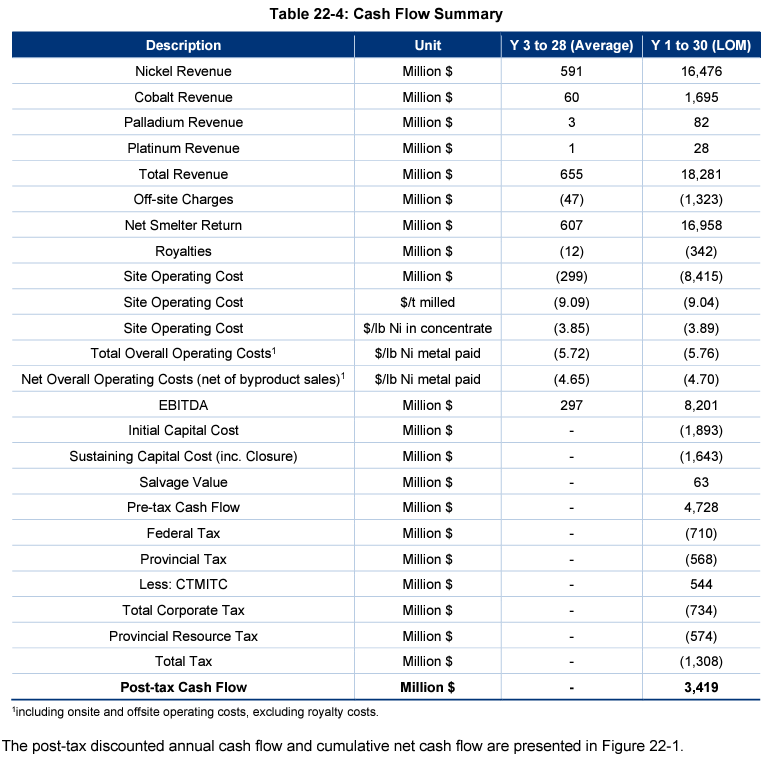

Table 22-4: Cash Flow Summary

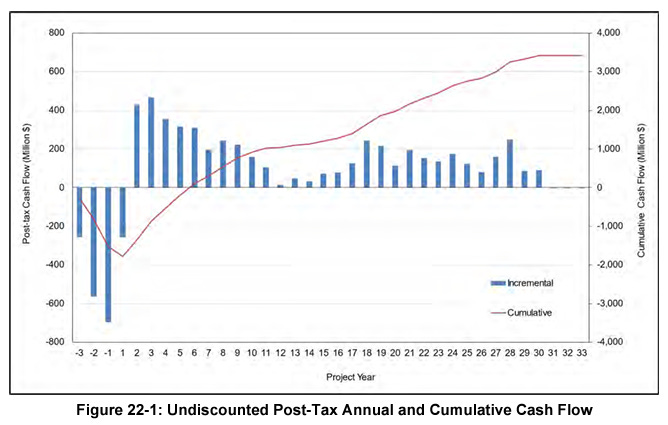

Figure 22-1: Undiscounted Post-Tax Annual and Cumulative Cash Flow

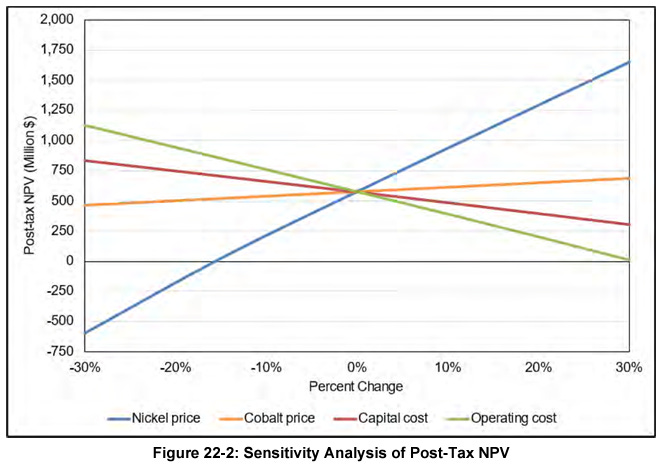

Figure 22-2: Sensitivity Analysis of Post-Tax NPV

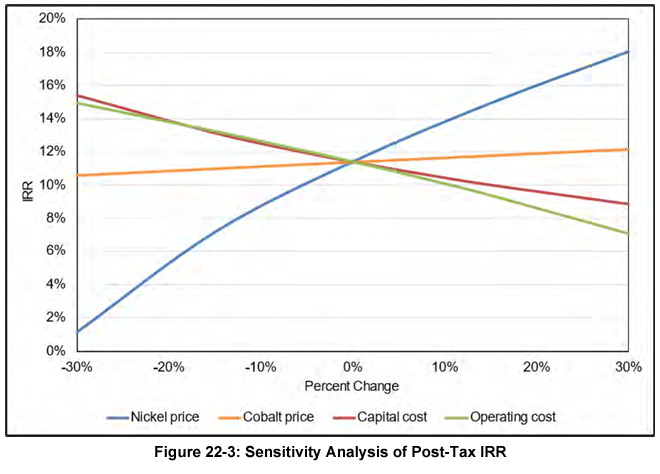

Figure 22-3: Sensitivity Analysis of Post-Tax IRR

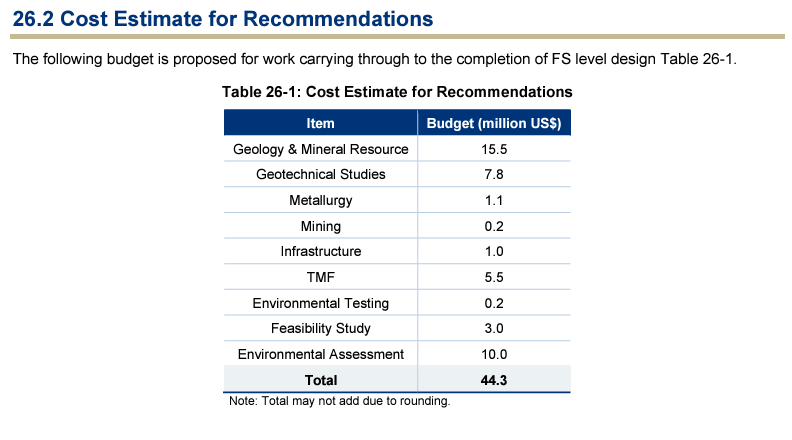

Table 26-1: Cost Estimate for Recommendations (to complete Feasibility Study)

Are you actually here? Did you actually make it? I… am impressed.

-Matthew from JRI

Let me know your thoughts! What sticks out to you?