Evaluating Matters: How to Value Fireweed Metals with PI Financial

Evaluating Matters: How to Value Fireweed Metals with PI Financial

I hosted analyst Connor Mackay to discuss Fireweed Metals. Connor explains why Fireweed is truly world-class and, paradoxically, why the market struggles to properly understand and value it.

I sat down with base metals analyst Connor Mackay of Pi Financial recently to discuss Fireweed Metals. Connor covers Fireweed and I took this opportunity to pick his brain and have him show his work a little bit on the process and logic behind his work.

Fireweed is a best-in-class asset that, because of this status, makes it a bit of a trick to properly place a dollar value on as it is without a true peer. However, its inherent and strategic value is impossible to ignore and as Fireweed continues to prove up discovery after discovery and progress through economic studies, you have to think that eventually a sort of critical mass will be achieved and its true value will be more properly reflected in its market cap and share price.

Part 1: Companion Article; Part 2: Written Summary and Transcript

FWZ.V; FOM.T; IVN.T

Part 1: Companion Article

Fireweed Metals sort of exists out on an island all on its own. Consider: It is a still-small $160m mc junior with not one, but two world-class projects in two separate niche-yet-critical metals (Macmillan Pass, or “Macpass” and zinc and Mactung’s tungsten). And these are early stage projects that don’t even have up-to-date economic studies attached to them and in terms of discovery are clearly just getting started.

This “problem” (what a problem to have) of having almost peerless projects in two niche metals makes Fireweed a challenge to place a proper value on. Even just one such project would be a challenge. But to have two, and then try to get both under a single big “value tent” really puts a wrench into efforts by investors, analysts, and the market in general.

How do you compare the incomparable? How do you do peer-based analysis on something that just might be peerless? Please note here that I am not trying to blow smoke in terms of implying some insane “to the moon” valuations with those rhetorical questions (though I do believe the true inherent value of Fireweed is clearly significantly higher than what the market is declaring it to be). Rather, I am wanting to emphasise just how hard it is to establish a value proposition for Fireweed.

But it is precisely the fact that it is so difficult to get a proper bead on Fireweed that makes it all the more critical to try. Because this isn’t actually some rhetorical “how many angels can dance on the head of a pin” thought exercise, but rather the most concrete and practical of needs - how to ascribe a dollar value onto something.

Which is why I enjoyed having the opportunity to sit down with Connor Mackay and talk shop on Fireweed last week. Connor has covered Fireweed for the better part of 6 months now in his position of base metals analyst at PI Financial, and wrote a very strong initiation-of-coverage report (which I provided the first 3 pages as a sample of above) last fall.

Connor’s work is data-backed and authoritative, working from known knowledge and reasonable, evidence-based extrapolations. Importantly for me, Connor’s work was also conservative in nature in a way not all paid analysis operates. He did extrapolate deposit sizes, but I believe did so responsibly (they will almost certainly end up much larger within a few more drill campaigns) and even used a 12% discount rate for his model when people wouldn’t have batted an eye had he gone with 10% or even 8%.

Take a look through the summary below to be able to pick out topics of interest to you, but Connor referenced a few things I felt was cogent.

First off, he shared his 3 core umbrella categories that drives the rest of his analysis:

Jurisdictional Support and Execution

Technical Expertise and Likelihood of Success

Ability to Finance

He also stated clearly that the 12% discount rate will fall to 10% and even lower as Fireweed completes economic and feasibility studies on Macpass and Mactung, meaning a primary chunk of remaining risk in the eyes of PI is “simply” getting the appropriate technical analysis and research completed.

He did touch on the 0.6 P/NAV ratio they use to help establish their price target, but I found I didn’t properly follow-up on asking him to anchor it to reality through proper peer comparisons. He did provide Foran Mining (FON.T) and Ivanhoe’s (IVN.T) Kipushi Zinc+Cu mine as a peer comp, so he did provide me some bread crumbs to go crunch that 0.6 P/NAV price myself. And I will do so at a later date.

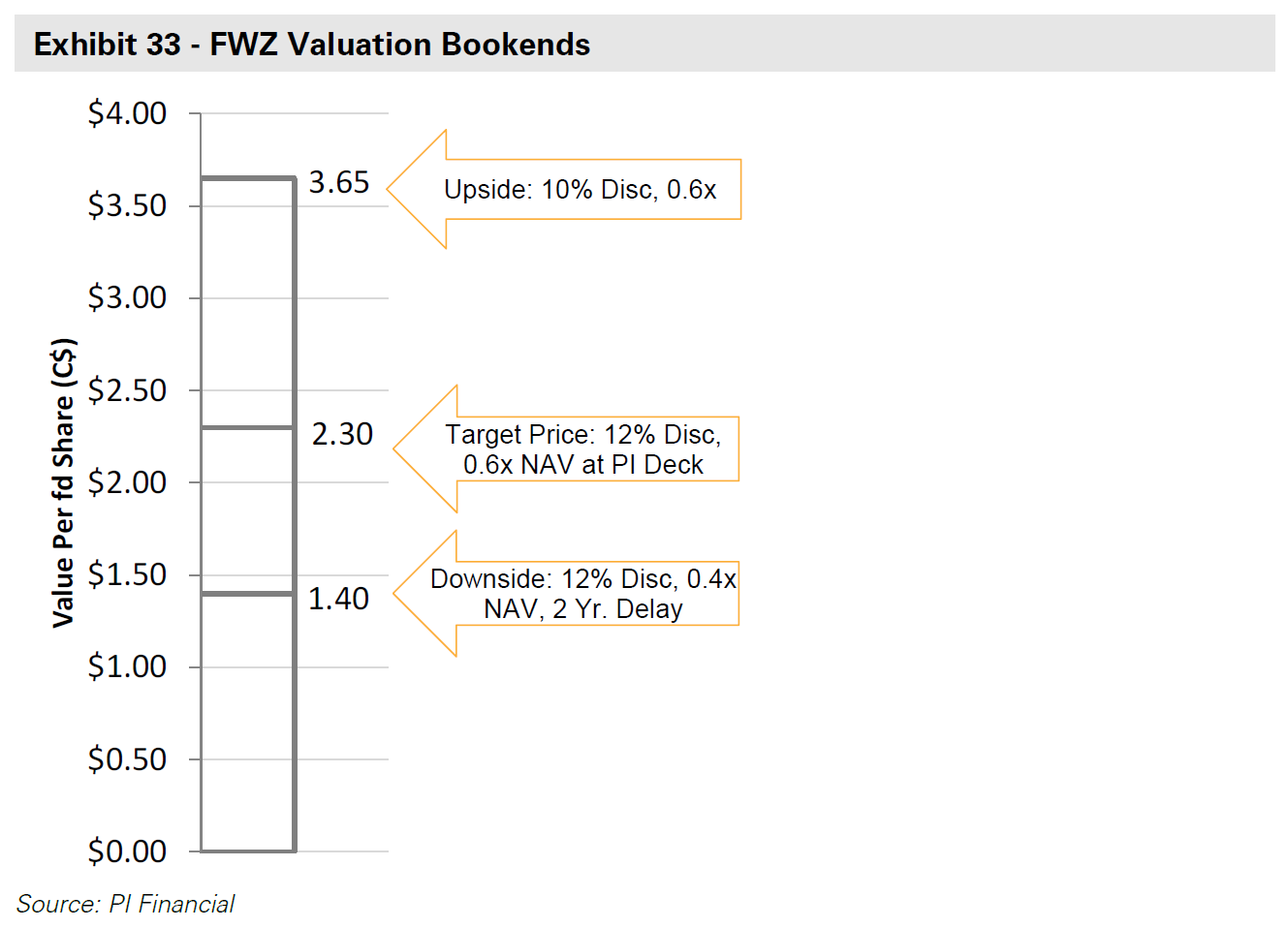

As for valuation and price targets, I have provided the summary of their analysis in the form of their valuation bookends and target price derivation tables below, coming up with a $2.30 target, and a range of $1.40-$3.65. See below.

I won’t belabour the point too much here. This was, for me anyway, an illuminating interview that helped shed some light on my understanding of how “the experts” go about their business in this industry. As someone who takes seriously always trying to learn more and be better at collecting, collating, and analysing the appropriate data through the appropriate lenses in this sector, it was an important 40 minute sit down. And I hope you do as well. Please provide feedback and suggestions if you would like to see more of this kind of interview, or topics and questions you might have for me!

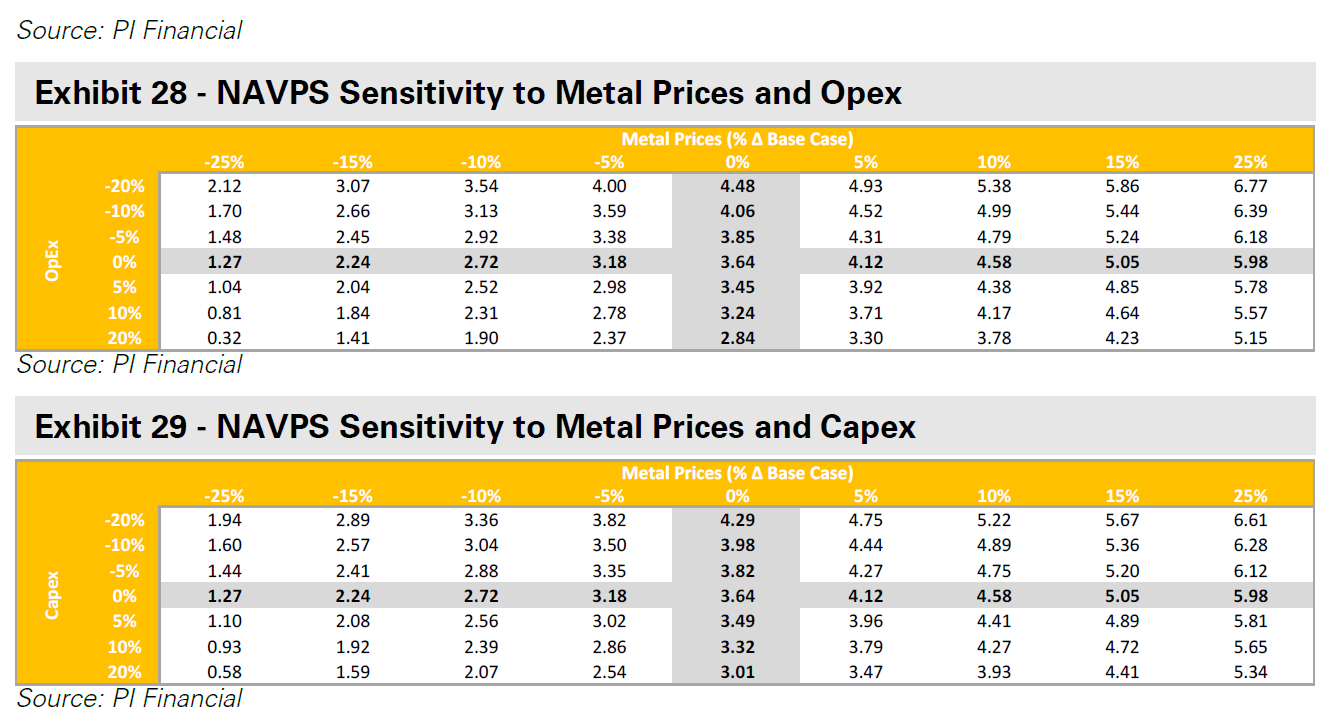

I am just about to board a plane to PDAC, so I will say goodbye for now. But before you go, check out the sensitivity charts (always one of my favourite parts of a PEA/PFS/FS) PI Financial has produced. And of course the written summary as well if that’s of interest for you.

Thanks for reading - and if you’re at PDAC, reach out to me. I would be happy to meet and have a chat.

Thanks for reading.

-Matthew from JRI

Part 2: Written Summary & Transcript

Link to Transcript

Click timestamps for link to video

02:21

Valuation Process: What are + & - do you look for?

Connor discusses the valuation process, emphasizing market awareness and engagement with management teams. Technical disclosures and transparency, as exemplified by Fireweed's open drill database, are highlighted as indicators of a company's integrity.

The conversation shifts to the importance of balancing project development and exploration upside. Fireweed's McMillan Pass property is cited as an example of potential growth beyond known deposits.

07:08

Risks and Opportunities the Market is Underestimating

They discuss the underestimated risks and opportunities in the market, focusing on the impact of costs, permitting timelines, and jurisdictional risks on valuation.

09:00

Connor's Key 3 factors in Risk Weighting

Connor elaborates on risk weighting, emphasizing jurisdictional, technical, and financing risks. Fireweed's valuation is discussed, with a focus on discount rates reflecting project-specific risks.

11:41

Use of 12% Discount Rate for Fireweed and Do Base Metals Deserve a Higher Rate than Precious?

The dialogue covers the rationale behind using a conservative 12% discount rate for Fireweed, considering its technical risk and potential for valuation adjustment as the project progresses.

They debate the industry tradition of applying higher discount rates to base metals projects compared to precious metals, considering inflation and cost pressures.

19:10

Why does Fireweed have such a disconnect between the low price and high value?

The discussion addresses the discrepancy between market valuation and inherent value in projects like Fireweed, exploring factors such as metal mix and market familiarity with specialty metals. Also explores the potential for government support in critical mineral projects.

23:23

The Zinc Market

They delve into the zinc market's supply constraints and Fireweed's unique position to address future demand, highlighting the importance of significant discoveries for project viability.

Discussing Fireweed's Gayna River project, they acknowledge its potential impact without currently ascribing value to it due to its remoteness and development challenges.

The conversation explores the zinc market's sensitivity to cost inputs and the potential for supply-side pressure to impact prices and demand.

31:00

Justifying their 0.6 NAV ratio they use as a price target and peer comparisons

They discuss Fireweed's valuation methodology, emphasizing the project's high-grade potential and the benefits of strategic investments for advancing exploration.

35:00

Core Remaining Risks and Upcoming Catalysts

The dialogue concludes with an overview of Fireweed's near-term expectations, including resource updates and economic studies, highlighting the project's technical and economic potential.

Valuation can be a maddening combination of qualitative and quantitative analysis. Maddening because ultimately the choice is yours as to which is value the most and where. Being able to host conversations such as this is critical in that it invites someone else into your thought process to provide suggestions and examples of how they do their own work for you to engage with and assess.

Regardless of the particular, individual metrics, though, Fireweed Metals remains one of the most compelling stories on the market.

Thanks for reading.

-Matthew from JRI